AI-Powered Backtesting: Key Features to Know

AI-Powered Backtesting: Key Features to Know

AI-powered backtesting tools are transforming how traders test and refine strategies. They address common pitfalls like overfitting, unrealistic assumptions, and data biases, ensuring strategies are better prepared for live trading. Here's what you need to know:

- AI Strategy Parsing: Converts plain-language trading ideas into MQL5 code, drastically reducing coding time. Example: Traidies automates this process, enabling quick strategy testing.

- Data Quality Controls: Tackles issues like lookahead and survivorship bias. Clean, accurate data is critical for reliable backtests.

- Scenario Simulations: AI identifies market regimes (bull, bear, volatile, etc.) and tests strategies under diverse conditions, including synthetic events like flash crashes.

- Hyperparameter Tuning: AI accelerates parameter optimization using methods like genetic algorithms and Bayesian optimization, while safeguards prevent overfitting.

- Execution Realism: Models slippage, spreads, and latency to reflect actual trading conditions. Stress testing ensures strategies can handle market frictions.

These features help traders minimize risks and improve strategy reliability. Tools like Traidies streamline the entire process, offering fast, efficient backtesting with realistic outcomes.

Backtest Any Trading Idea Using AI Agentic Skills - No Coding Needed

sbb-itb-3b27815

1. Traidies: AI Strategy Parser and MQL5 Code Generation

Traidies tackles a common challenge for traders: turning strategy ideas into testable code. Manually coding strategies in MQL5 can be a slow, expertise-heavy process, creating a gap between brainstorming and actual testing. Traidies bridges this gap with its AI Strategy Parser, which converts plain-language trading strategies directly into MQL5 Expert Advisor (EA) code.

Here’s how it works: traders simply describe their strategies in everyday language - something like, "Buy when the 50 EMA crosses above the 200 EMA and RSI is below 60; exit when the price drops 2%." The AI then translates this description into fully functional MQL5 code, complete with built-in order management using libraries like Trade.mqh.

What’s the benefit? Traditional workflows for coding and testing strategies can take weeks, sometimes even months. With Traidies, this process is reduced to just minutes. Once the code is generated, the platform's backtesting engine runs the strategy on historical data, delivering key performance metrics almost instantly. This creates a seamless loop from idea to validation, allowing traders to quickly test multiple strategies, identify the most promising ones, and focus on refining them. For active traders, this means more time spent on improving strategies and less on the technical grind.

2. AI-Driven Data Cleaning and Quality Controls

AI-powered code generation has revolutionized testing speeds, but the reliability of results still hinges on the quality of the data. Backtests are only as strong as the data they rely on. Issues like missing data points, unadjusted stock splits, or gaps from contract rollovers can mislead AI models. As the saying goes: garbage in, garbage out.

One major pitfall is lookahead bias, which occurs when models inadvertently use future data - like dividends or full-dataset normalization - that wouldn’t have been available at the time of trading. A 2024 study published in the Review of Financial Studies revealed that addressing this bias significantly lowered the average Sharpe ratio reported in machine learning-based trading strategies. This underscores how backtest results can paint a very different picture compared to real-world performance.

Another challenge is survivorship bias, which quietly skews results. For instance, between 2000 and 2025, about 45% of the S&P 500's companies were replaced. If your backtest only includes companies that are still active today, it’s essentially a "winners-only" perspective. AI systems counter this by sourcing data from point-in-time databases like CRSP or Compustat, which include delisted, bankrupt, and acquired companies. This approach ensures the historical dataset reflects reality, not just the success stories.

"The performance of any AI crypto trading bot is only as good as the data it was trained and tested on." - Dwight Sproull, Former Content Lead, 3Commas

Maintaining temporal integrity is another critical factor. AI models use chronological splits and avoid using samples that are too close to the test window. Techniques like purged cross-validation and embargo gaps help achieve this. For example, professional quants often recommend a 5–10 trading day embargo gap for daily models to prevent information leakage. In futures trading, AI also applies proportional back-adjustment to continuous contracts, which smooths out artificial price jumps caused by contract rollovers. These methods create a stronger, more reliable dataset, ensuring backtests are better equipped for the challenges of live market conditions.

3. Scenario Simulation and Market Regime Detection

AI tools have advanced to the point where they can simulate a wide range of market conditions, but the foundation for these simulations lies in using clean, unbiased data. While having bias-free data is critical, the testing process must also account for a variety of market scenarios.

Modern AI frameworks can automatically classify historical data into distinct market phases - think bull, bear, sideways trends, accumulation, distribution, high-volatility, and even news-driven events. Why does this matter? Because strategies that perform well in calm, bullish markets might completely fall apart in volatile or bearish conditions. By breaking down market regimes, AI allows traders to assess performance metrics like the Sharpe ratio, maximum drawdown, and Sortino ratio for each specific phase. This approach highlights weaknesses that might otherwise be hidden in an overall performance score. These classifications also lay the groundwork for more advanced stress-testing and performance evaluation techniques.

Beyond just analyzing historical data, AI frameworks can create synthetic scenarios. Using techniques like GANs (Generative Adversarial Networks), they generate realistic market conditions and even simulate extreme events, such as flash crashes or liquidity shortages, to test risk management strategies under pressure.

Walk-Forward Analysis is another powerful tool in the mix. This technique trains on one segment of data and tests on the next, untested segment, offering insights into how strategies might perform in unknown future conditions. Pair that with Monte Carlo simulations, which resample historical trade data, and traders gain a clearer picture of potential worst-case outcomes. Together, these methods complement AI-driven data improvements, creating a more comprehensive and realistic backtesting process.

"Backtesting explains the past. Algorithmic backtesting AI explains what survives the future." - FintorAI

One practical takeaway: always test your strategy's sensitivity. If a small increase in assumptions for slippage or spreads causes performance to collapse, your strategy’s edge may be too fragile for real-world application. Advanced AI frameworks include this kind of friction testing in their regime simulations, ensuring potential weaknesses are identified long before real money is at stake.

4. Hyperparameter Optimization with AI

Hyperparameter optimization takes strategy refinement to the next level by leveraging AI to streamline what used to be a painstakingly manual process. In the past, setting key parameters for trading strategies could take hours - or even days - of trial and error. Now, AI-powered tools can evaluate between 200 and 600 parameter combinations in just seconds. This speed not only saves time but also allows for deeper and more precise optimization.

Two standout techniques dominate this space. The first is genetic algorithms (GAs), like NSGA-II, which are inspired by the principles of biological evolution. These algorithms create a "population" of parameter sets, select the best-performing ones, and then combine and mutate them to generate new, improved combinations over multiple iterations. The second approach, Bayesian optimization, takes a more strategic route. It learns from each test result and focuses on the most promising areas, avoiding the inefficiency of testing every possible combination. Together, these methods accelerate the optimization process and enhance risk management by helping traders select parameters with care.

However, all this power comes with a potential pitfall: overfitting. This occurs when a strategy performs brilliantly on historical data but falls apart in live markets. A major red flag here is a backtested Sharpe Ratio exceeding 3.0, which is almost always a sign of overfitting. To counter this, AI employs several safeguards:

- Walk-Forward Analysis (WFA): This method optimizes parameters on one data window and then validates them on a separate, unseen window. A WFA efficiency score above 70% is a strong indicator of reliability.

- Deflated Sharpe Ratio: This adjustment accounts for the number of parameter combinations tested, filtering out strategies that may have simply "gotten lucky".

- Parameter Limits: Restricting strategies to three or four optimizable parameters significantly reduces the risk of overfitting.

By combining these techniques, AI ensures that optimized strategies remain robust and better reflect live market conditions.

"An AI model with a Sharpe Ratio above 3.0 in backtesting is almost certainly overfitted." - Technical Analysis Pro

One practical tip is to focus on broad plateaus in parameter heatmaps. These represent zones where nearby parameter values yield similarly strong results, indicating robust performance. In contrast, isolated peaks often signal quirks in historical data rather than genuine strategy strength. This disciplined approach to parameter selection complements earlier steps in data integrity and scenario analysis, creating a more reliable foundation for live trading.

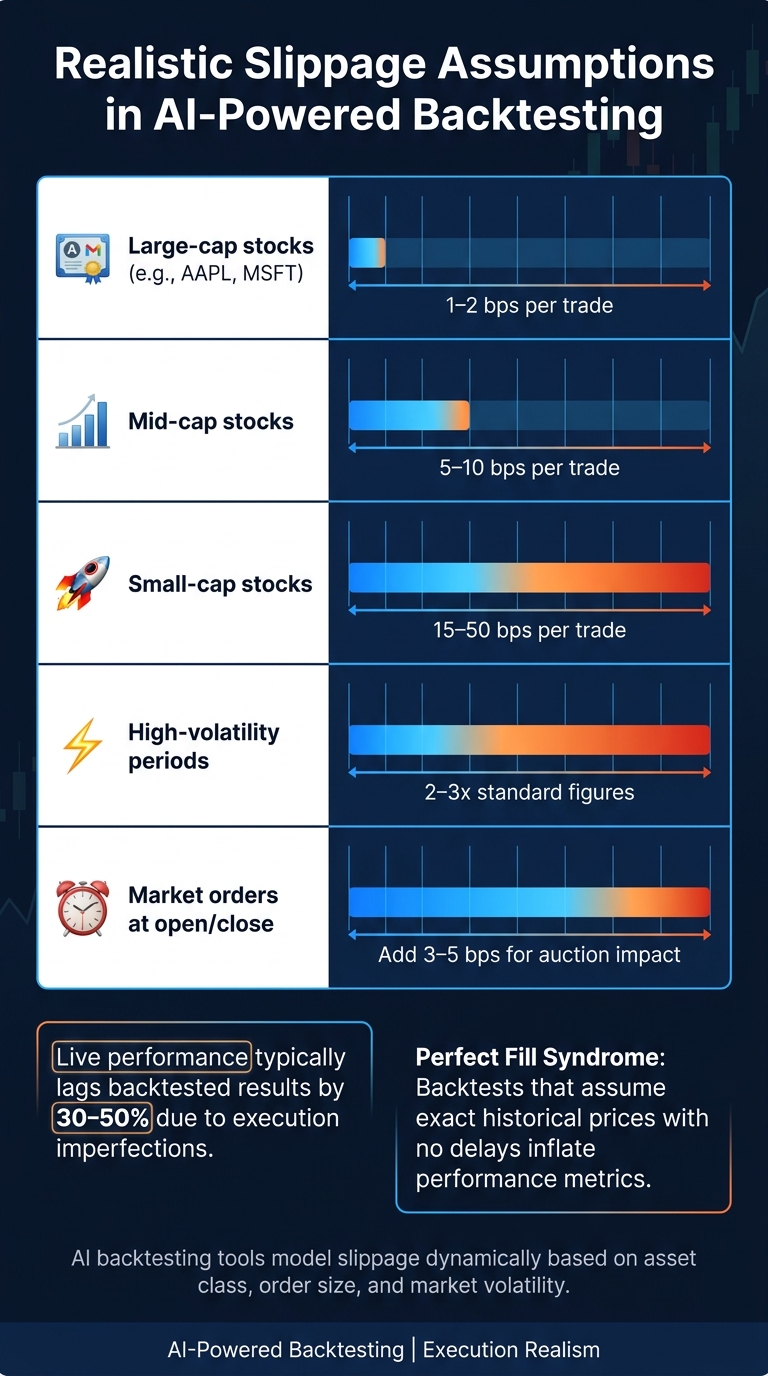

5. Risk Management and Execution Realism

AI Backtesting: Realistic Slippage Assumptions by Asset Class

Once you've refined your data and fine-tuned parameters, the next step is ensuring your strategy can handle the messy reality of live markets. This is where risk management and realistic execution modeling come into play.

Even the best backtested strategy can crumble in live trading if it overlooks market frictions. A common pitfall is "perfect fill syndrome", where backtests unrealistically assume trades execute at exact historical prices, with no delays and unlimited liquidity.

AI-powered backtesting tackles this by accounting for three major friction points: slippage, spreads, and execution latency. Slippage, for instance, isn’t treated as a fixed cost. Instead, it varies based on factors like asset class, order size, and market volatility. To put it in perspective, slippage can range from 1–2 basis points (bps) for large-cap stocks like AAPL or MSFT, up to 15–50 bps for small-cap stocks. And during periods of high volatility, those figures can double or triple to reflect real-world conditions.

| Asset Class / Condition | Realistic Slippage Assumption |

|---|---|

| Large-cap stocks (e.g., AAPL, MSFT) | 1–2 bps per trade |

| Mid-cap stocks | 5–10 bps per trade |

| Small-cap stocks | 15–50 bps per trade |

| High-volatility periods | 2–3x standard figures |

| Market orders at open/close | Add 3–5 bps for auction impact |

Execution delays are another critical factor, especially for strategies that rely on fast signals, such as those based on news sentiment. AI tools simulate the time lag between a signal firing and the actual order execution. A good rule of thumb: if a trade condition is confirmed at the close of a candle, the backtest should enforce entry on the next candle. This simple adjustment eliminates a major source of inflated performance metrics.

To further test the robustness of a strategy, cost stress testing is used. By deliberately increasing slippage and fee assumptions, you can expose weaknesses in the model. This is crucial because live performance typically lags behind backtested results by 30–50%, thanks to execution imperfections and model decay. Dynamic modeling like this ensures your strategy is ready for real-world trading challenges, preserving the integrity of AI-driven development.

"Backtesting is not about proving you are right. It is about discovering where you are wrong before the market charges you for it." - Kevin Goldberg, AIPredictiveSignals.com

These principles of risk management and realistic execution set the stage for a detailed comparison of AI-powered backtesting platforms.

Feature Comparison Table

Here's a breakdown of how Traidies brings AI-driven backtesting to the table:

| Feature | Traidies |

|---|---|

| Strategy Generation | AI Strategy Parser transforms natural language into MQL5 EA code |

| Data Quality / Depth | Dukascopy candlestick data for Forex, crypto, equities, and commodities |

| Scenario Simulation | Integrates economic calendar and multi-timeframe logic for event testing |

| Optimization Method | Automated backtesting engine delivers performance metrics on historical data |

Key Features of Traidies

Traidies simplifies the journey from idea to execution by converting natural language strategy descriptions into MQL5 code. This means traders can deploy strategies in MetaTrader 5 without any coding knowledge. Additionally, its integration with an economic calendar allows users to test scenarios around major news events, like Non-Farm Payrolls.

Conclusion

AI-powered backtesting has redefined strategy validation by addressing common challenges like overfitting, unrealistic fills, and untested market conditions. By incorporating enhanced data cleaning, scenario simulations, and parameter tuning, it bridges the gap between theoretical performance and actual trading outcomes.

Key tools such as walk-forward analysis, regime detection, and accurate slippage modeling play a vital role in creating more reliable backtests. These features ensure that strategies aren't just optimized for past data but are also prepared for the unpredictable nature of live markets.

For those looking to implement these principles without diving into code, Traidies provides an accessible solution. Its AI Strategy Parser can take plain-language strategy descriptions and convert them into MQL5 code. Combined with its automated backtesting engine, you can test strategies on historical Dukascopy data across forex, crypto, equities, and commodities. Even better, you can get started with 3 free backtests daily, no credit card needed.

The end goal isn’t just to create a backtest that looks profitable on paper. It’s to develop a strategy that performs when real money is at stake.

FAQs

How can I tell if my backtest is overfitted?

A backtest might be overfitted if its performance takes a sharp dive when applied to out-of-sample data, reports overly optimistic metrics (like a Sharpe ratio exceeding 3.0), or reacts dramatically to minor tweaks in parameters. These red flags suggest the model may be picking up on random noise instead of identifying genuine, actionable patterns.

What data biases can make results look better than real trading?

Data biases, such as survivorship bias and lookahead bias, can distort backtesting outcomes. Survivorship bias happens when failed assets are excluded from the analysis, leading to an incomplete picture of performance. On the other hand, lookahead bias involves using future information that wouldn’t have been accessible during actual trading. Both biases can result in overly optimistic performance estimates, making the results appear more favorable than they truly are.

How should I model slippage and spreads for realistic backtests?

When running backtests, it's crucial to account for slippage and spreads to reflect real market conditions. These factors depend on variables like liquidity, volatility, and the size of your orders. For instance, large-cap stocks might experience slippage of 1-2 basis points, while smaller stocks can face much higher rates, especially during volatile periods.

To stay on the safe side, consider overestimating slippage by 20-50% to prepare for unexpected market events. Additionally, make sure your spread modeling is dynamic - spreads tend to widen when liquidity is low or markets are more volatile. This approach helps create a more realistic simulation of trading conditions.