Bayesian vs. Grid Search: Hyperparameter Tuning in Trading

Bayesian vs. Grid Search: Hyperparameter Tuning in Trading

Hyperparameter tuning is critical for optimizing trading strategies, but not all methods are created equal. Here's the difference:

- Grid Search is exhaustive but computationally expensive. It tests all possible combinations of parameters, making it ideal for smaller parameter spaces (2–3 variables) and quick backtests.

- Bayesian Optimization is smarter and more efficient. It uses past trials to predict better parameter combinations, excelling in larger, complex spaces (5–15 variables) or when backtests are slow.

Key takeaway: Use grid search for simplicity and transparency in small setups. Opt for Bayesian optimization when working with multiple parameters or noisy data. For best results, combine both - start broad with grid search, then refine with Bayesian optimization.

Quick Comparison

| Factor | Grid Search | Bayesian Optimization |

|---|---|---|

| Search Strategy | Exhaustive (all combinations) | Predictive (guided search) |

| Parameter Space | Best for 2–3 variables | Best for 5–15 variables |

| Efficiency | Computationally expensive | More efficient |

| Noise Handling | Limited | Strong |

| Transparency | High | Lower |

Pro Tip: Always validate results with techniques like Purged K-Fold to avoid overfitting, especially in trading where data is noisy and markets are dynamic.

Challenges of Hyperparameter Tuning in Trading Models

Common Trading Models and Their Hyperparameters

Trading models, whether they rely on machine learning algorithms or technical systems, come with various hyperparameters that influence critical trading metrics. For instance, random forests require adjustments to parameters like learning rate, number of trees (n_estimators), maximum depth, and minimum samples per leaf. Meanwhile, technical models depend on settings such as lookback windows, entry/exit thresholds, and volatility multipliers.

The sheer number of hyperparameter combinations can quickly become overwhelming. Imagine a random forest model with four hyperparameters, each offering five potential values. That setup alone results in 625 combinations. Add 5-fold cross-validation, and you're looking at 3,125 model fits.

| Hyperparameter | Model Type | What It Controls |

|---|---|---|

| Learning Rate | ML (gradient boosting, neural nets) | Step size during optimization; too high causes instability |

| Lookback Window | Time-series, technical indicators | How far back the model "looks" for signals |

| Max Depth / Leaf Size | Tree-based ML models | Model complexity; deeper trees risk overfitting noise |

| Entry/Exit Thresholds | Rule-based, technical strategies | Values that trigger buy or sell signals |

Trading-Specific Constraints to Keep in Mind

Tuning trading models introduces unique challenges compared to standard machine learning tasks, particularly due to the stakes and constraints involved.

Financial data is noisy. Unlike domains like image recognition or spam filtering, financial markets are dominated by noise, making it easy to mistake random fluctuations for meaningful patterns. A hyperparameter search that is too aggressive can lead to overfitting noise rather than uncovering real signals. As Marcos López de Prado explains:

"In finance, the signal-to-noise ratio is low, non-stationarity is the norm, and the cost of overfitting is measured in capital. Every degree of freedom in a pipeline is an opportunity to overfit."

Additionally, markets are dynamic. A configuration that performs well during periods of low volatility may fail miserably during high-volatility phases.

Another major issue is data leakage. Traditional k-fold cross-validation methods often fall short in financial contexts because they don't account for overlapping labels, such as triple-barrier labels. This overlap can unintentionally leak future information into the training data, inflating validation scores that won't hold up in live trading. To address this, techniques like PurgedKFold introduce a time gap between training and validation sets, effectively preventing leakage.

Finally, multiple testing bias is a significant concern. The more hyperparameter combinations you test, the higher the likelihood of stumbling upon a configuration that looks promising purely by chance.

These complexities make automation a necessity for efficient and reliable hyperparameter tuning.

How Automation Helps with Tuning

Manually testing hundreds - or even thousands - of hyperparameter combinations is simply not feasible. Automation simplifies and accelerates the process, integrating hyperparameter tuning seamlessly into the strategy development workflow.

Platforms like Traidies offer a streamlined approach by combining AI-driven strategy generation, MQL5 code output, and automated backtesting in one unified system. Traders can describe their strategy in plain language, generate the corresponding code, and instantly backtest it against historical data - eliminating the need for repetitive manual coding.

Automation also enables pruning, which involves halting trials that show poor performance early on, saving valuable computational resources. By discarding underperforming configurations after just a few iterations, traders can significantly cut down on the time and effort required for evaluations. This level of efficiency is crucial for overcoming the challenges outlined above.

sbb-itb-3b27815

Grid Search: How It Works and When to Use It

How Grid Search Works

Grid search is a simple yet systematic approach to hyperparameter tuning. It works by evaluating every possible combination of parameters within a predefined range. This process involves defining parameter ranges, calculating all combinations (using the Cartesian product), backtesting each configuration on historical data, and identifying the one with the best performance metrics. Because of its deterministic nature, grid search consistently delivers the same results when repeated under identical conditions.

"The appeal of grid search lies in its simplicity and thoroughness. You're guaranteed to find the best combination within your predefined grid." – ML Journey

One of its strengths is the ability to predict the exact number of evaluations required. For instance, if you're tuning three parameters with 5, 4, and 3 candidate values, grid search will perform exactly 60 evaluations. This predictability is especially useful in trading scenarios where precision and structure are critical.

Where Grid Search Works Well in Trading

Grid search is particularly effective for trading strategies with a small number of hyperparameters. Its transparency and ease of auditing make it ideal for workflows with 2–3 key parameters, such as moving average lengths or Bollinger Band deviations. Since every combination is tested and logged, the process is highly traceable - an advantage for meeting compliance requirements. Traders often use 2D heatmaps to visualize how different parameter combinations affect metrics like total profit.

A common practice is to start with a coarse grid that uses broad increments to identify promising regions. Once these regions are identified, a finer grid can be applied to zero in on the best-performing configurations. This "coarse-to-fine" method balances thoroughness with efficiency.

However, while grid search excels in certain scenarios, it does have its drawbacks.

Limitations of Grid Search

One major drawback is the risk of combinatorial explosion. Adding even a single extra hyperparameter with 5 values can increase the number of evaluations from 60 to 300, making the process computationally expensive. Another limitation is that grid search treats each trial independently, ignoring insights from previous evaluations. This can lead to wasted computational resources, as it may repeatedly test clearly suboptimal regions. For example, a Random Forest case study revealed that grid search required 810 trials to find the optimal configuration, which was only discovered on the 680th iteration. In contrast, Bayesian optimization achieved the same result in just 67 iterations.

There’s also the risk of overfitting, especially when using highly granular grids or limited historical data. This can result in tuning that captures noise rather than meaningful patterns. To address this, robust validation strategies like out-of-sample testing and walk-forward analysis are essential. Without these safeguards, grid search can become inefficient, particularly in fast-changing trading environments where timely optimization is critical.

Bayesian Optimization: A More Directed Tuning Method

How Bayesian Optimization Works

Unlike grid search, which methodically tests every possible combination, Bayesian optimization takes a smarter approach. It builds a surrogate model - often a Gaussian Process (GP) or Tree-structured Parzen Estimator (TPE) - to predict performance and guide the search. An acquisition function, such as Expected Improvement or Upper Confidence Bound, then focuses on areas likely to yield the best results. Essentially, it acts like a dynamic map of the search space, improving accuracy with each trial.

What sets Bayesian optimization apart is its ability to learn from each trial. Instead of starting over every time, it balances exploitation (fine-tuning regions that already show promise) with exploration (testing uncertain areas for potential improvements).

"Bayesian logic mimics how markets operate in the real-world – updating our beliefs as new information comes in." – Dan Buckley, Head Market Analyst, DayTrading.com

This approach doesn’t just make the process more efficient - it fundamentally changes how optimization is done, as explained below.

Where Bayesian Optimization Has an Edge

Bayesian optimization shines in scenarios where exhaustive methods like grid search fall short. For instance, grid search becomes unwieldy as the number of hyperparameters increases. Testing five values across four hyperparameters means evaluating 625 combinations - or 3,125 model fits when using 5-fold cross-validation. Bayesian optimization avoids this exponential growth by targeting evaluations to regions most likely to yield good results.

This makes it particularly effective for continuous parameters - like learning rates or regularization strengths - where a grid might miss the best value that lies between predefined points. It’s also better at handling noisy data, such as financial market signals, because the surrogate model accounts for uncertainty, making it easier to separate meaningful patterns from random noise.

For example, in a 2019 experiment by Sergey Malchevskiy, the hyperopt package was used to optimize a trading strategy with four hyperparameters over 300 iterations and five one-month folds of historical Bitfinex data. The optimizer identified strong objective values of -15.45 and -9.72 for ETH/BTC and XMR/BTC, respectively, while filtering out unprofitable assets like LTC/BTC before validation.

Limitations of Bayesian Optimization

Despite its strengths, Bayesian optimization isn’t perfect. Each iteration requires updating the surrogate model and optimizing the acquisition function, which adds computational complexity.

While the method reduces the number of trials and, by extension, Multiple Testing Bias, it doesn’t inherently prevent overfitting. Techniques like walk-forward analysis and using a separate holdout dataset are still necessary to ensure robustness.

"Bayesian optimization does not actively 'prevent' overfitting; it simply reduces Multiple Testing Bias by requiring fewer trials." – Arthur, Quantitative Researcher

These considerations are crucial when implementing Bayesian optimization in automated trading systems that must adapt to ever-changing market conditions.

Basic Search vs. Bayesian Optimization | Hyperparameter Optimization

Bayesian Optimization vs. Grid Search: A Direct Comparison

Grid Search vs. Bayesian Optimization: Hyperparameter Tuning for Trading

Key Factors to Compare

Let’s break down the main differences between Bayesian optimization and grid search by focusing on computational cost, noise handling, and transparency.

Computational cost is one of the most noticeable differences. Grid search becomes exponentially more expensive as you add parameters. Meanwhile, Bayesian optimization uses a surrogate model to strategically pick the next trial, often achieving excellent results in just 20–50 evaluations.

Noise handling is another area where these methods diverge. Grid search assumes each backtest result is definitive, which can lead to mistaking random fluctuations for optimal settings. Bayesian optimization, however, employs probabilistic models to account for uncertainty, reducing the risk of overfitting to noise.

Transparency is also worth mentioning. Grid search produces a comprehensive, auditable record of all parameter combinations tested, making it easier to document and explain - especially in regulated settings. On the other hand, Bayesian optimization can feel more opaque, as its probabilistic decision-making process is harder to trace.

"The search problem is only as good as the validation objective. Bayesian HPO cannot rescue a bad target." – ml4trading.io

Which Method Fits Which Trading Scenario

Depending on the situation, one method may be a better fit than the other.

Grid search is ideal for scenarios with 2–3 hyperparameters, quick backtests (lasting just seconds), and a need for complete reproducibility. For example, when fine-tuning a simple moving average crossover strategy with just two parameters (fast and slow periods), grid search’s exhaustive approach can be a good match.

Bayesian optimization works better in more demanding situations, such as when backtests are slow, the parameter space includes 5–15 hyperparameters, or the data is particularly noisy. A practical approach is to start with a random search to identify promising areas, then use Bayesian optimization for fine-tuning.

"The goal is not to find the hyperparameters that win on one validation window... it is to find a configuration that survives temporal instability, search noise, and finite trial budgets." – ml4trading.io

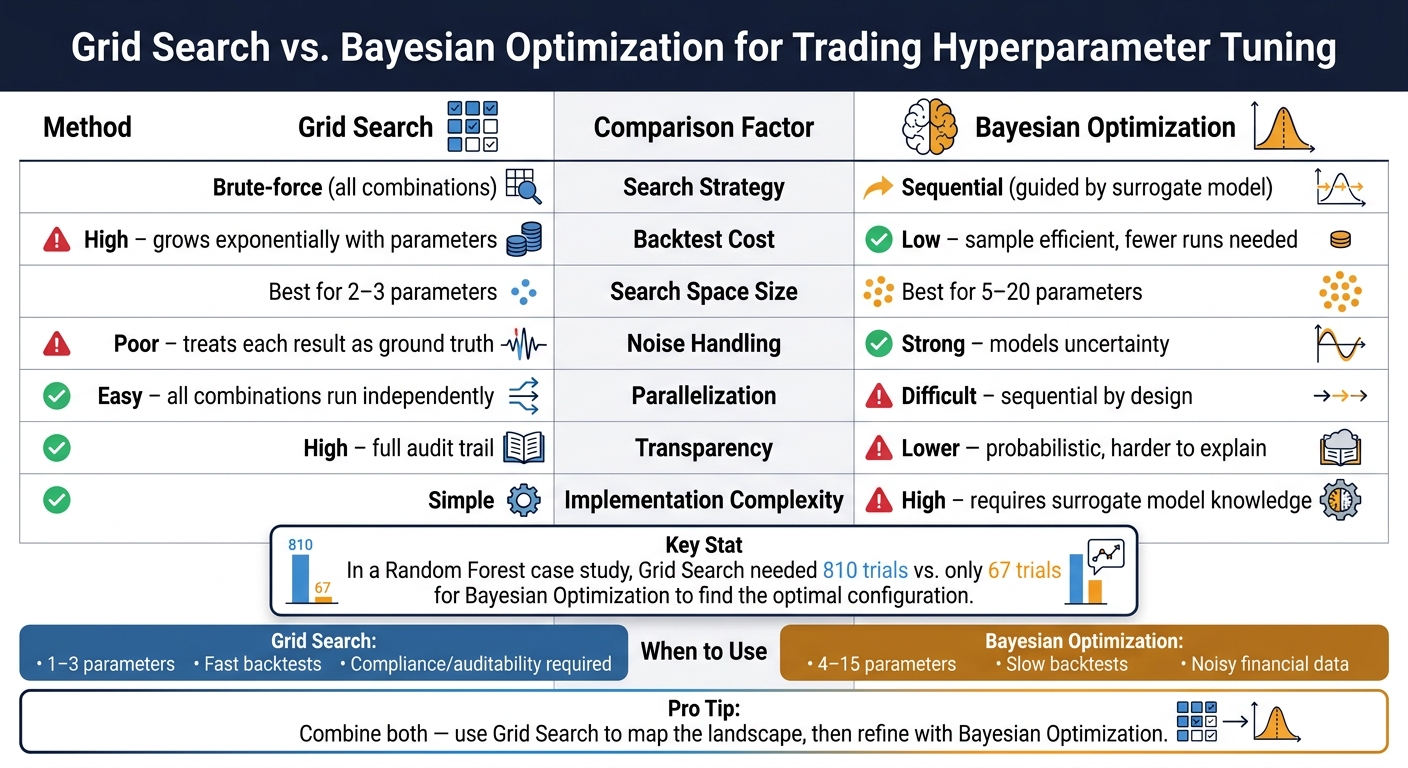

Comparison Table: Bayesian Optimization vs. Grid Search

| Factor | Grid Search | Bayesian Optimization |

|---|---|---|

| Search Strategy | Brute-force | Sequential |

| Backtest Cost | High – grows exponentially with parameters | Low – sample efficient, fewer runs needed |

| Search Space Size | Best for 2–3 parameters | Best for 5–20 parameters |

| Noise Handling | Poor – treats each result as ground truth | Strong – models uncertainty |

| Parallelization | Easy – all combinations run independently | Difficult – sequential by design |

| Transparency | High – full audit trail | Lower – probabilistic and harder to explain |

| Implementation Complexity | Simple | High – requires surrogate model knowledge |

For example, in a Random Forest case study, Bayesian optimization identified optimal parameters much faster than grid search. This efficiency is especially important for trading strategies where backtests can be extremely time-consuming. These comparisons highlight which method is better suited for building an effective and reliable trading strategy.

Adding Tuning Methods to Automated Trading Workflows

A Step-by-Step Automated Trading Workflow

Creating an efficient workflow is crucial for automated trading. Start by defining your strategy and its parameters, then set a clear objective, such as maximizing the Sharpe ratio. Once that's done, initialize the optimizer, conduct iterative backtests, and deploy the configuration that performs best. Begin with a coarse grid search to identify promising parameter regions, and then use Bayesian optimization to refine those results further.

Persistent storage plays a vital role in this process. By saving your optimization study in a SQLite or PostgreSQL database, you can ensure that your work survives crashes, supports parallelization, and provides a detailed audit trail. This is especially important in regulated trading environments, where maintaining a complete record of every trial is often mandatory. Following this structured approach not only boosts reliability but also enhances the speed of your automated systems.

How Traidies Supports Hyperparameter Tuning

Traidies makes integrating hyperparameter tuning into your trading workflow straightforward by automating key processes like strategy parsing and backtesting. Typically, managing strategy code, backtesting, and optimization requires juggling multiple tools. Traidies eliminates that complexity by combining AI-powered strategy parsing, automated MQL5 code generation, and historical backtesting into one platform.

With Traidies, traders can describe their strategies in plain language, generate the corresponding Expert Advisor code, and run backtests - all without switching between tools. The effectiveness of your optimization largely depends on the speed and reliability of your backtests. Faster, automated backtesting allows you to conduct more trials within a limited time, improving the results of both grid search and Bayesian optimization.

Best Practices for Trading Optimization

Adopting a few key principles can ensure consistent performance improvement in your automated trading workflow while avoiding pitfalls like overfitting.

First, always use Purged K-Fold cross-validation to prevent data leakage. Next, carefully consider your objective function:

"If your objective function is a statistical measure on labelled data... use Optuna. If it is a financial measure on historical equity curves... do not. Optuna's advantage in HPO is the same property that makes it dangerous for strategy optimization - it finds the optimum too reliably." – MetaTrader 5 / MQL5

Finally, embed your tuning process within a walk-forward framework. This involves re-optimizing your strategy on a rolling window of recent data while validating it on a separate, untouched holdout set. This approach keeps your strategy aligned with current market conditions, avoiding reliance on outdated historical data.

Conclusion and Practical Guidelines

Key Takeaways

Grid search and Bayesian optimization play distinct roles in refining trading models. Grid search is straightforward and easy to interpret but struggles with scalability, while Bayesian optimization identifies optimal settings more efficiently, often requiring only about 20 trials to pinpoint a solution. To put it into perspective, testing a 10-parameter grid could demand millions of combinations. However, excessive testing risks overfitting, where the "winning" configuration may succeed by chance rather than revealing a genuine trading edge. As Marcos López de Prado explains:

"Overfitting often stems from flawed validation processes rather than the optimizer itself."

This highlights the critical role of robust validation in ensuring reliable results, regardless of the optimization method used. These factors lead to actionable advice for selecting the best tuning approach.

How to Choose Between the Two Methods

The decision largely hinges on the size of your parameter space and the cost of backtesting. For smaller, clearly defined spaces - typically involving 1–3 parameters - grid search offers simplicity and ease of implementation. However, when dealing with 4 or more parameters, lengthy backtest durations, or complex, noisy search spaces (common in real-world trading), Bayesian optimization tends to outperform.

A hybrid approach can be particularly effective: begin with a broad grid search to map out the parameter landscape, then zero in on the most promising region using Bayesian optimization. This combination works well with the robust validation techniques discussed earlier, helping your model stay aligned with the unpredictable nature of markets. To avoid bias, always maintain an out-of-sample holdout set.

FAQs

What objective metric should I optimize for a trading strategy?

When fine-tuning models, it's crucial to prioritize an out-of-sample risk-adjusted performance metric, like the Sharpe ratio or Sortino ratio (inverted if you're working with minimization). To tackle overfitting, assess performance across multiple folds or time periods. Any fold showing negative performance should be penalized to ensure more reliable results.

For better accuracy, use a weighted mean of the fold scores, placing greater emphasis on those closer to the out-of-sample period. This approach ensures the optimizer focuses on meaningful improvements during hyperparameter tuning.

How many backtests are needed to trust the 'best' parameters?

When it comes to Bayesian optimization, there isn’t a hard-and-fast rule for the number of trials to run. A good starting point is to conduct some random initial trials and then validate the best parameters across multiple temporal folds. In practice, about 100 trials are commonly used, but you’ll often see results stabilizing after 60–70 iterations.

What’s more important than the exact number of trials is ensuring the robustness of your findings. Always confirm your model’s ability to generalize by evaluating it on out-of-sample data. Prioritize fold-based reliability over simply hitting a specific trial count to achieve dependable outcomes.

How do I prevent data leakage and overfitting during tuning?

To prevent issues like data leakage and overfitting, opt for nested, purged, or embargo-aware time-series cross-validation rather than standard k-fold methods. Make sure that your train and test label windows remain distinct, avoiding any overlap. When assessing trials, use fixed temporal folds to maintain consistency. Only choose the optimal configuration after the entire search process is complete, and then conduct a final evaluation using data that has not been touched during training. If you incorporate pruning or early stopping, ensure that intermediate metrics align with the same temporal boundaries as the final evaluation.