When to Use Grid Search or Random Search in Backtesting

When to Use Grid Search or Random Search in Backtesting

Choosing between grid search and random search for backtesting boils down to the size of your parameter space and your computational resources. Here's a quick breakdown:

- Grid Search: Best for small parameter spaces (2–3 parameters). It systematically tests all combinations but can become computationally expensive as parameters increase. Ideal when you have time and resources to ensure thorough testing.

- Random Search: Great for large or complex parameter spaces. It randomly samples combinations, making it faster and less resource-intensive. While it may not find the absolute best settings, it often delivers good results efficiently.

The key is balancing thoroughness and efficiency. Start with random search to identify promising ranges, then refine with grid search for precision.

Quick Comparison

| Feature | Grid Search | Random Search |

|---|---|---|

| Approach | Exhaustive | Random Sampling |

| Best for | Small parameter spaces | Large or complex spaces |

| Efficiency | Computationally intensive | Faster, fixed iterations |

| Risk of Overfitting | Higher | Lower |

| Reproducibility | Deterministic | Stochastic (unless seeded) |

Both methods have their strengths, and a hybrid approach often works best: use random search to scout the parameter space, then apply grid search to fine-tune.

Grid Search vs Random Search: Complete Comparison for Trading Backtests

Advanced Stock Backtesting in Python (Grid Search with FLAML)

sbb-itb-3b27815

What Is Grid Search in Trading Backtests

Grid search is a method that systematically evaluates every possible combination of predefined parameter values - essentially forming a Cartesian product - and tests them against historical data. For example, if you're optimizing an EMA crossover strategy with two parameters, each having 10 possible values, grid search would run 100 backtests to cover all combinations. This approach ensures that the best-performing combination within the defined parameter grid - essentially the global optimum in this finite and discrete space - is identified. Understanding how this process works step by step is key to applying it effectively.

How Grid Search Works

The process begins by creating a grid, which is defined by setting ranges and step sizes for each parameter. For example, you might test RSI periods ranging from 10 to 20 in increments of 2, alongside RSI entry thresholds ranging from 25 to 35 in steps of 5. This setup results in 6 RSI period options and 3 threshold options, yielding a total of 18 combinations. Each of these combinations is then backtested against historical data, with results ranked based on key performance metrics like the Sharpe ratio. Secondary filters - such as requiring a minimum number of trades or limiting maximum drawdown - are often applied to ensure the strategy is practical and tradable.

A typical workflow involves starting with a coarse grid, using broader ranges and larger steps to identify promising regions. Once these regions are found, a finer grid with smaller step sizes can be applied to zero in on the optimal settings. With this process in mind, it's useful to weigh the strengths and weaknesses of grid search.

Pros and Cons of Grid Search

One of the biggest advantages of grid search is its exhaustive nature - it ensures that every possible configuration within the defined parameter space is tested, leaving no stone unturned. Its simplicity and reproducibility make it a reliable tool, especially when dealing with a limited number of parameters. For strategies focusing on 2–3 core parameters, the computational requirements are manageable, and the risk of overfitting remains relatively low.

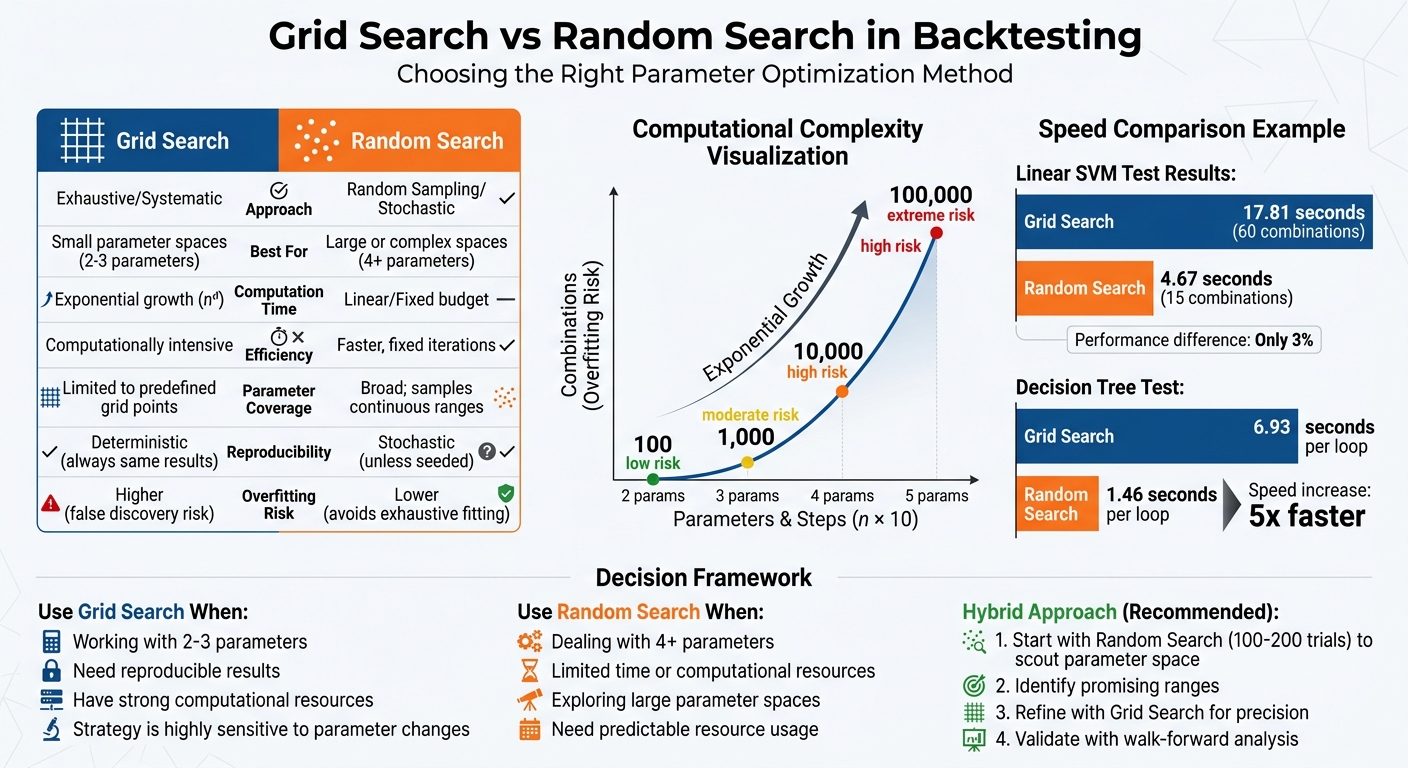

However, grid search has its downsides, particularly when dealing with more complex strategies. The computational load increases dramatically as the number of parameters and their respective steps grow, a phenomenon often called the "curse of dimensionality." The complexity follows the formula n^d, where n is the number of values per parameter and d is the number of parameters. For instance, while 2 parameters with 10 steps each result in 100 combinations, adding three more parameters with the same steps balloons the total to 100,000 combinations, significantly increasing the risk of overfitting.

Another limitation is that grid search only evaluates specific points on the grid. If the true optimal value lies between these predefined steps, it might be overlooked. Testing thousands of combinations also raises the likelihood of "false discovery", where the selected parameters align with historical noise rather than representing a meaningful market edge.

| Parameters | Steps per Param | Total Combinations | Overfit Risk |

|---|---|---|---|

| 2 | 10 | 100 | Low |

| 3 | 10 | 1,000 | Moderate |

| 4 | 10 | 10,000 | High |

| 5 | 10 | 100,000 | Extreme |

What Is Random Search in Trading Backtests

Random search offers a different approach from grid search by sampling a subset of parameter combinations randomly instead of testing every single option. While grid search systematically evaluates all possible combinations, random search focuses on efficiency, especially in scenarios involving many parameters. By doing so, it avoids the computational burden of exhaustively testing every possibility, making it a practical choice for high-dimensional tuning.

This method is especially useful when the parameter space is large. For example, a grid search involving five parameters with 10 steps each would require 100,000 backtests. In contrast, random search allows you to set a manageable number of tests - say 500 or 1,000 - while still exploring a wide range of parameter values. This flexibility makes it a powerful tool for traders who need to balance exploration with computational limits.

How Random Search Works

The process starts with defining parameter ranges for each variable in your strategy. For instance, you might allow RSI periods to vary between 10 and 30, entry thresholds from 20 to 40, and stop-loss percentages between 1% and 5%. From these ranges, the system randomly selects a fixed number of combinations to test - say 200.

Each selected combination is then backtested against historical data. The results are ranked based on your chosen performance metrics, and the best-performing combination is identified as the optimal configuration. The beauty of this approach lies in its flexibility: you can control the number of tests to fit your computational resources while still covering a broader parameter space than grid search would at a similar cost.

"If we are the RandomizedSearchCV, we will try some of the combinations that are randomly picked, take a picture and choose the best performer at the end." – Gustavo Santos

In practice, random search often outpaces grid search in terms of execution time. For example, when the number of parameter options increased from 12 to 48, grid search times jumped from about 18 seconds to over 60 seconds. Meanwhile, random search times stayed steady at around 10 seconds. Despite this speed difference, the final error metric differed by only 3%, showing that random search can achieve near-optimal results much faster.

Pros and Cons of Random Search

Random search stands out for its computational efficiency. For example, in a Decision Tree test, grid search took 6.93 seconds per loop for 48 combinations, whereas random search completed the same task in just 1.46 seconds - a nearly 5x speed increase. This efficiency is especially valuable for strategies combining multiple indicators, where grid search would otherwise require thousands of backtests.

Another advantage is its ability to handle the "curse of dimensionality." Instead of getting bogged down in exhaustive evaluations, random search samples across the entire parameter space. Research by Bergstra and Bengio confirms that random search is often more effective for hyperparameter optimization in high-dimensional spaces. In one study, random search identified its best-performing set in just 36 iterations out of a possible 100 trials.

However, random search does have its limitations. The method doesn't guarantee finding the absolute best parameter combination because it relies on chance. If the random samples miss certain high-performing regions, those opportunities might go unnoticed. That said, these "missed" peaks often represent overfitting to historical noise rather than true market patterns.

"Random search is suitable if you're willing to sacrifice performance in exchange for fewer iterations and smaller run time." – Aashish Nair, Towards Data Science

Another drawback is that random search doesn't learn from past trials. Each test is independent, so the method doesn't focus on promising regions once they’re identified. Because of this, many traders use random search as a first step to locate promising parameter ranges. They then refine these results with a more targeted grid search for further optimization.

Grid Search vs Random Search: Comparison Table

Here's a side-by-side look at how grid search and random search stack up:

Comparison Table

| Feature | Grid Search | Random Search |

|---|---|---|

| Approach | Systematic / Exhaustive | Stochastic |

| Computation Time | Exponential growth (n^d) | Linear / Fixed budget (n_iter) |

| Parameter Coverage | Limited to predefined grid points | Broad; can sample continuous ranges |

| Best Use Case | Small search spaces (few parameters) | Large or high-dimensional spaces |

| Reproducibility | Deterministic | Stochastic |

| Overfitting Risk | High (risk of "false discovery") | Lower (avoids exhaustive fitting) |

Grid search and random search differ significantly in their approach, efficiency, and risk levels. Grid search systematically tests all combinations of predefined parameters, but this exhaustive method causes its computation time to grow exponentially with the number of parameters and grid points. In contrast, random search operates within a fixed number of iterations, making it more time-efficient, especially for larger or more complex parameter spaces.

Another important distinction lies in reproducibility. Grid search consistently produces the same results for the same inputs, making it deterministic. Random search, on the other hand, introduces variability unless a fixed random seed is used.

Overfitting is also a critical factor to consider. Grid search's exhaustive nature can lead to overfitting, as it might latch onto noise in the data rather than meaningful patterns. Random search, by sampling parameter spaces more broadly and less systematically, reduces this risk.

These differences highlight when each method is most effective. Choosing the right approach depends on the size of your parameter space and your specific optimization goals. Stay tuned to discover when to apply grid search or random search for the best results in your backtesting strategy.

When to Use Grid Search

Grid search shines when you're working with just a couple of key parameters. Let’s say your trading strategy involves tuning a moving average period and a stop-loss percentage - grid search is a great fit here. Amit Yadav from Biased-Algorithms explains it well:

"If your hyperparameter space is small and manageable, Grid Search is the perfect tool. You won't feel the computational cost as much, and you can confidently say you've tested all possibilities."

One of grid search's biggest advantages is reproducibility. Since it’s deterministic, running the same backtest with identical parameters will always yield the same results. This is particularly useful when verifying performance or collaborating with a team. In contrast, random search generates different outcomes each time unless you set a fixed random seed.

If you have strong computational resources and plenty of time, grid search becomes even more appealing. It’s "embarrassingly parallel", meaning you can split the workload across multiple processors or cloud resources to accelerate the process. For example, a momentum strategy with five parameters required testing 7,000 combinations. On a standard consumer-grade laptop, this took about an hour.

Grid search is also ideal for strategies with high sensitivity to parameter changes, where testing every combination is necessary to find the best settings. However, as the number of parameters increases, the combinations grow exponentially, which can lead to overfitting.

To get the most out of grid search, keep the following tips in mind:

- Focus on two or three core parameters to avoid an unmanageable grid size.

- Use wider steps (e.g., increments of 5 instead of 1) to reduce the total combinations.

- Once you identify optimal parameters, fine-tune them slightly. A sharp drop in performance during fine-tuning often signals overfitting, meaning you've hit an isolated "peak" rather than a stable "plateau".

When to Use Random Search

Grid search works well for small parameter sets, but random search shines when dealing with larger, more complex spaces. Here's why: as the number of parameters increases, the total combinations grow exponentially. For example, with five parameters, each having 10 possible values, you’re suddenly looking at 100,000 combinations - this is where grid search struggles to keep up.

One of the biggest advantages of random search is its predictable resource usage. You can decide in advance how many trials you want to run - whether it's 100 or 200 - and know exactly how much time and computational power it will require. This is especially useful if you're working on a standard laptop or trying to manage cloud computing costs. Plus, random search's broad sampling increases the chances of hitting on the parameters that matter most, as some have a much greater impact on performance than others. As machine learning researcher Amit Yadav points out:

"Random Search often finds good solutions faster than Grid Search - especially in higher-dimensional search spaces."

If you're pressed for time, random search is a faster option. For instance, in a test using linear SVM, random search evaluated 15 parameter combinations in just 4.67 seconds, while grid search took 17.81 seconds to assess 60 combinations. Data scientist Aashish Nair explains:

"The random search is suitable if you're willing to sacrifice performance in exchange for fewer iterations and smaller run time."

This speed makes random search a great choice when you're working with limited time or computational resources.

Think of random search as a scouting tool. Use it to explore your parameter space and identify promising regions. Once you've narrowed things down, you can switch to grid search to fine-tune those specific areas. To make your random search more effective, consider setting a minimum threshold - such as 50 to 100 trials - to avoid mistaking lucky outliers for genuinely good parameter combinations.

How to Choose the Right Method on Traidies

To make the most of Traidies' backtesting tools, consider blending random search and grid search methods. Start with a random search to quickly scan the parameter space, then move to a grid search to refine and confirm the most promising results. This two-step process helps you save time while reducing the risk of overfitting.

Begin by running a random search with a set iteration limit. This approach allows you to explore a wide range of parameters without overloading your computational resources. Once the random search identifies promising combinations, shift gears. As Santos explains, random search helps pinpoint starting points for a more focused grid search.

When you’ve identified a high-performing range, use a grid search to test values in that specific area. For instance, if the random search suggests that an EMA period of 20 works well, set up a grid search to test values between 15 and 25. This targeted approach avoids the massive time costs of testing the entire parameter space, while zeroing in on the optimal settings.

Next, verify the stability of your chosen parameters by testing small variations. If slight changes result in significant performance drops, you’re likely dealing with an overfitted peak rather than a reliable market edge. As Quanthop points out:

"If your best parameter set is surrounded by poor-performing neighbors, it is almost certainly overfit... Real edges form plateaus - broad regions where nearby values produce similar, positive results."

Keep your strategy practical by limiting the number of parameters you optimize. Aim for 2 to 3 key parameters, as strategies with more than 4 can easily fall into overfitting traps. Finally, validate your results with walk-forward analysis to ensure your parameters work across varying market conditions. For statistical significance, your backtest should include at least 50 to 100 trades.

Conclusion

When deciding between grid search and random search, the choice largely depends on the number of parameters you’re optimizing and the computing resources at your disposal. Grid search shines when dealing with two or three parameters, providing a thorough and systematic exploration that ensures you identify the best combination within a defined range. However, its computational requirements increase exponentially with more parameters, making it less practical in high-dimensional scenarios. Random search, on the other hand, is well-suited for exploring larger parameter spaces. By sampling random combinations within a fixed budget, it becomes a more efficient option when optimizing four or more parameters.

Both methods, however, share a common risk: overfitting. As Quanthop cautions:

"If your best parameter set is surrounded by poor-performing neighbors, it is almost certainly overfit... Real edges form plateaus - broad regions where nearby values produce similar, positive results".

To mitigate this, validation through walk-forward analysis is essential, regardless of the optimization method you select.

A hybrid approach often provides the best of both worlds. Begin with random search to quickly identify promising regions, then refine those areas with a focused grid search. This combination balances efficiency with precision while reducing the likelihood of overfitting. Additionally, narrowing optimization to two or three critical parameters - and ensuring stability by testing small adjustments - can result in more reliable configurations.

Ultimately, the goal isn’t just to find optimal parameter sets for historical data but to identify robust configurations that can adapt to various market conditions and timeframes. This approach helps avoid chasing fleeting patterns and focuses on achieving consistent performance.

FAQs

How many random-search trials are enough?

When tuning hyperparameters in trading strategies, running a few hundred random-search trials is often enough to cover the parameter space effectively. Generally, starting with 100 to 300 trials is a good benchmark. However, the exact number can vary depending on how complex your parameter space is and how robust you want the results to be. Be ready to adjust the number of trials based on the specific needs and goals of your strategy.

How do I spot overfitting during optimization?

Overfitting happens when a strategy excels with historical data but struggles when applied to new, unseen data. To spot it, methods like walk-forward analysis and out-of-sample testing are essential. Key warning signs include a noticeable performance gap between in-sample and out-of-sample results or inconsistent performance across varying market conditions. To prevent this, steer clear of overly intricate parameter adjustments and prioritize strategies that deliver steady results across a range of datasets.

Should I optimize parameters on multiple timeframes?

When it comes to optimizing parameters, it's best to stick to a single timeframe rather than juggling multiple ones at once. Techniques like grid search perform more efficiently when working with fewer parameters and within a defined timeframe. Trying to optimize across multiple timeframes not only complicates the process but also raises the likelihood of overfitting. To ensure your backtesting is both manageable and dependable, concentrate on refining parameters within one timeframe at a time.