How to Automate Counterparty Risk Adjustments

How to Automate Counterparty Risk Adjustments

Counterparty risk is the chance that a trading partner fails to meet their obligations, potentially leading to financial losses. Manual risk management methods often fall short due to errors, delays, and the inability to handle vast amounts of market data. Automation, powered by AI, offers a better way to manage this risk in real time.

Here’s the key takeaway: AI-driven systems can monitor creditworthiness 24/7, analyze massive datasets, and adjust risk strategies instantly. Tools like Traidies simplify the process, converting plain-language instructions into executable trading code (MQL5). This minimizes errors, reduces response time, and protects against counterparty failures.

Steps to Automate Counterparty Risk Adjustments:

- Collect and organize data (financial health, market risk, compliance).

- Train AI models to predict risks like probability of default.

- Use platforms like Traidies to create automated trading bots.

- Set dynamic risk controls (e.g., position sizing, stop-loss rules).

- Test and refine strategies regularly to align with market changes.

5 Steps to Automate Counterparty Risk Adjustments in Trading

How to Create Real Time Counterparty Risk Algotrading Strategy

sbb-itb-3b27815

What is Counterparty Risk in Automated Trading

Counterparty risk (CCR) refers to the possibility that a trading partner might fail to meet their contractual obligations, potentially causing both financial losses and harm to your reputation. In the fast-paced world of automated trading, where transactions happen in milliseconds, risks can escalate before they’re even detected. Real-time monitoring becomes essential, as sudden liquidity shortages or credit downgrades can set off a chain reaction of defaults in mere hours. For example, during periods of market volatility, a 24-hour delay in addressing risks could increase uncollateralized exposure by 0.5%–1.0% of the $650 trillion derivatives market.

"To react quickly to unexpected market events, we need real-time analysis on vast amounts of both in-flight and historic data." – ADSS

Without automation, relying on manual methods leaves traders vulnerable, unable to respond swiftly to emerging threats. To effectively manage these risks, it’s crucial to understand their core components.

Main Elements of Counterparty Risk

Counterparty risk can be broken down into three primary components:

- Exposure at Default (EAD): The total amount expected to be owed if a default occurs.

- Probability of Default (PD): The likelihood of a counterparty defaulting within a specific timeframe.

- Loss Given Default (LGD): The portion of the exposure that would be lost after considering collateral recovery.

These components come together in a widely used formula:

Expected Loss (EL) = PD × LGD × EAD.

Take this example: if your exposure is $100,000, the default probability is 5%, and you expect to recover 40% of the exposure through collateral, your estimated loss would be around $3,000. Automated systems are designed to continuously update these metrics in response to changing market conditions.

Collateral plays a crucial role as a safety net, offering assets that can be liquidated in case of default. However, it’s not a perfect solution. The collapse of Archegos Capital Management in March 2021 illustrates this point. Major banks suffered over $10 billion in losses, partly due to hidden leverage tied to total return swaps. These examples highlight the importance of dynamic, automated systems to adjust counterparty exposure in real time.

Problems with Manual Risk Adjustments

In high-speed trading environments, manual methods for managing counterparty risk simply can’t keep up. Tools like spreadsheets or periodic reviews are too slow when trades are executed in milliseconds. Even minor errors, such as a mistyped formula, can lead to massive exposure. Manual processes also struggle to consolidate data from multiple markets and manage the sheer volume of information, making it nearly impossible to maintain a clear, comprehensive view of risk.

Another critical limitation of manual methods is their inability to address "wrong-way risk." This occurs when a counterparty’s likelihood of default increases alongside market volatility, exposing you to the greatest losses at the worst possible times.

"The exposure is highest when the counterparty is most likely to default. In other words, defaults are more likely when the financial impact would be the greatest." – KX

Automated systems are indispensable for overcoming these challenges, ensuring that risks are identified and managed in real time.

Preparing for Automation

To automate counterparty risk adjustments effectively, start by building high-speed trading platforms and organizing your data for machine learning. Without these foundational steps, automation efforts are likely to fall short.

As of 2026, only 39% of organizations are currently using artificial intelligence for risk management, with another 24% planning to adopt it within two years. Starting now gives you a clear advantage. Let’s explore the platforms, tools, and data preparations you’ll need to set up automation successfully.

Platforms and Tools You Need

To automate trading and risk management, you’ll need a platform capable of 24/7 operation, paired with AI-driven tools to transform your risk strategies into actionable code.

MQL5 (MetaQuotes Language 5) is a key tool for automated trading. It allows you to create Expert Advisors (EAs) that monitor the markets, execute trades with precision, and backtest risk strategies. The platform’s built-in Strategy Tester helps you evaluate hedging and risk parameters using historical data, ensuring your settings are optimized before going live.

"Automated systems execute trades faster and with greater accuracy than manual trading, essential for capturing fleeting hedging opportunities." – Trading Strategies Academy

However, coding in MQL5 requires technical knowledge that not all traders possess. This is where tools like Traidies come in. Traidies simplifies the process by converting plain-language instructions into MQL5 code. For instance, you could describe a rule like, “Reduce position size by 50% when the counterparty credit rating drops below BBB,” and the platform will generate the necessary code automatically.

Beyond trade execution, you’ll also need AI-enabled GRC (Governance, Risk, and Compliance) platforms. These systems handle vendor onboarding, real-time risk scoring, and continuous monitoring to ensure your automation remains compliant and secure.

Getting Your Data Ready

Automation isn’t just about tools - it’s also about having the right data. Machine learning models require three key types of data: historical market data, real-time price feeds, and well-organized datasets that combine both structured and unstructured information.

Historical market data - such as OHLC prices, ATR volatility, and trading volume across timeframes - is critical for backtesting. For the most accurate results, use “every tick based on real ticks” instead of relying solely on OHLC data. This approach captures intra-bar movements and liquidity gaps, which are often missed with less detailed data. To avoid errors, verify broker-provided data against independent sources like Dukascopy or TickData.

Real-time feeds are equally important, providing up-to-the-minute insights into your trading account and market conditions. This includes metrics like account equity, balance, margin requirements, and cumulative profit/loss, tracked over daily, weekly, and monthly intervals. Additionally, live bid/ask spreads and volatility measurements help you stay informed about current market dynamics.

Organized datasets must handle both structured data (e.g., market prices, claims) and unstructured data (e.g., PDFs, handwritten notes, news articles) to create a full picture of risk. In MQL5, you can use global variables to maintain persistent states across platform restarts, structures (struct) to manage multi-dimensional data, and arrays to track multiple indicator values. External data, like major economic news (e.g., FOMC, NFP, CPI releases), can be incorporated using APIs such as Alpha Vantage.

Finally, establish strong data governance policies to maintain the integrity of your information, especially when handling sensitive third-party data. Before executing trades, validate all inputs to ensure there are no errors, such as zero or negative values in account balances or risk percentages, which could lead to calculation issues.

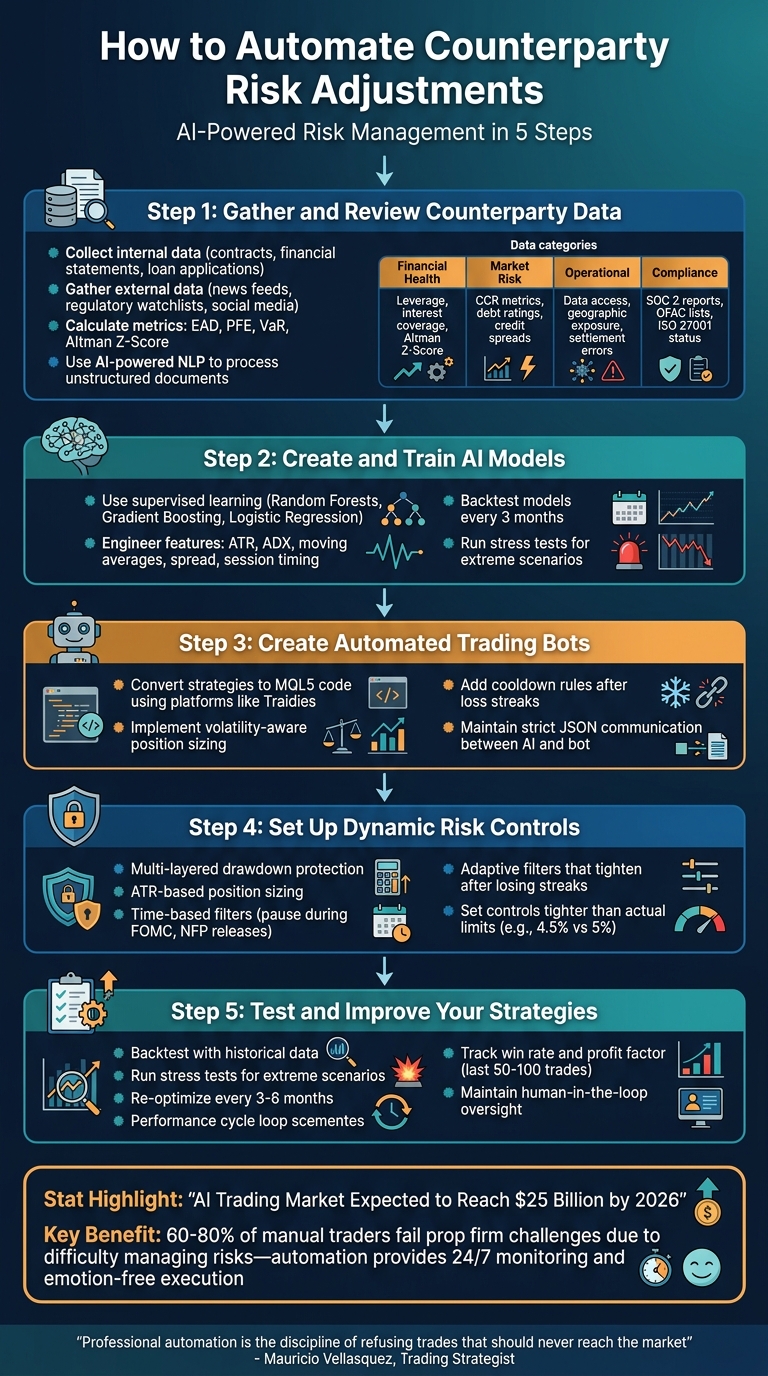

How to Automate Counterparty Risk Adjustments

Implementing an automated system for counterparty risk adjustments involves a series of steps that build on one another. By leveraging real-time data and advanced tools, you can create a framework that continuously adapts to changing risk conditions.

Step 1: Gather and Review Counterparty Data

Start by collecting data from various internal and external sources. Internal data includes contracts, financial statements, and loan applications. External sources might involve news feeds, financial records, legal databases, social media, and regulatory watchlists like OFAC.

The third-party risk management market is expanding rapidly. To streamline data extraction, use AI-powered Natural Language Processing (NLP). This can help process unstructured documents like vendor questionnaires, SOC 2 reports, and insurance certificates. For instance, in 2025, the University of Kentucky's Information Technology Services Cybersecurity team used AI to summarize SOC 2 reports, cutting down on manual work and costs.

Once you’ve collected the data, calculate metrics like EAD (Exposure at Default), PFE (Potential Future Exposure), and VaR (Value at Risk) for model training. Additionally, use the Altman Z-Score to assess bankruptcy risk:

Z = 1.2(Working Capital/Assets) + 1.4(Retained Earnings/Assets) + 3.3(EBIT/Assets) + 0.6(Market Value of Equity/Liabilities) + 1.0(Sales/Assets).

| Data Category | Specific Data Points | Purpose |

|---|---|---|

| Financial Health | Leverage, interest coverage, Altman Z-Score | Assess bankruptcy risk and creditworthiness |

| Market Risk | CCR metrics, debt ratings, credit spreads | Evaluate market risk exposure |

| Operational | Data access, geographic exposure, settlement errors | Highlight operational vulnerabilities |

| Compliance | SOC 2 reports, OFAC lists, ISO 27001 status | Ensure regulatory and security alignment |

Once your data is organized, you’re ready to train your AI models.

Step 2: Create and Train AI Models

Develop supervised learning models to predict default probabilities and exposure levels. Algorithms like Random Forests, Gradient Boosting Machines, or logistic regression are effective for uncovering patterns in credit data. These models refine risk metrics over time, enabling better trading decisions.

Instead of raw data, use engineered features like ATR (Average True Range), ADX (Average Directional Index), distance from moving averages, spread, session timing, and recent loss streaks for training. For real-time applications, platforms like MetaTrader 5 (MT5) can send structured data to a private server, where an AI model processes it and returns a JSON response with key fields such as signal, confidence, and reasoning. This ensures the AI acts as a "context filter" rather than an independent decision-maker.

"AI algorithms are only as good as the data on which they are trained, making it essential to continuously audit and refine models to ensure fairness and accuracy."

– Richa Tiwari, TrustCloud

Regularly backtest your models - at least every three months - to verify their ability to predict exposures and defaults accurately. Stress testing is equally important to assess performance under extreme scenarios like macroeconomic shocks or liquidity crises.

With your models ready, the next step is to translate strategies into automated actions.

Step 3: Create Automated Trading Bots

Convert your risk strategies into executable code using tools like Traidies, which can transform plain-language instructions into MQL5 code. For example, instruct the system to "Reduce position size by 50% when the counterparty credit rating drops below BBB", and the platform will generate the necessary code.

Incorporate volatility-aware position sizing that adjusts based on your risk percentage and ATR to account for market changes. Add cooldown rules to pause trading after a series of losses, preventing impulsive "revenge trading". Use global variables to store critical risk states, such as daily profit and loss, ensuring the system retains its limits even after a restart.

Maintain strict JSON communication between your AI model and trading bot. As Mauricio Vellasquez explains:

"The machine can advise the strategy, but the risk engine must govern it."

– Mauricio Vellasquez

Your risk engine should always have the final say, overriding AI-generated signals when necessary.

Now, it’s time to implement dynamic risk controls.

Step 4: Set Up Dynamic Risk Controls

Establish multi-layered drawdown protection and adaptive position sizing using ATR-based controls and time-based filters. Studies show that 60–80% of participants in prop firm challenges fail due to the difficulty of manually managing risks and drawdowns.

Dynamic position sizing can help by reducing exposure after losses and increasing it during winning streaks. Use volatility-adjusted controls to set stop-loss levels, take-profit targets, and trailing stops that reflect current market conditions.

Incorporate time-based risk mitigation with "News Filters" that pause trading during high-impact events, such as FOMC or NFP releases, to avoid extreme volatility. Adaptive filters can also tighten requirements after losing streaks to minimize further risks.

In February 2024, Yapi Kredi, a Turkish bank, introduced AI-powered automation for tasks like document collection and transaction checks. Their system flags exceptions for human auditors, demonstrating how automation can enhance efficiency while maintaining oversight.

Before going live, ensure your strategies are thoroughly tested.

Step 5: Test and Improve Your Strategies

Before deploying your system, backtest it extensively with historical data. Set tighter controls than your actual limits - for example, 4.5% instead of 5% - to account for slippage and execution delays.

Run stress tests alongside backtests to evaluate performance under extreme scenarios. This step is critical for ensuring your system can withstand sudden market shocks and volatility.

Finally, keep a "human-in-the-loop" approach. Human oversight should remain central for reviewing AI-generated insights, especially for critical decisions and exceptions.

Once your system is fine-tuned, you’ll have a robust framework ready for live deployment.

Best Practices for Automating Counterparty Risk

To keep your automated risk management system effective, you need to adapt it as market conditions and counterparty profiles shift. These practices help ensure your system stays reliable and avoids hidden pitfalls.

Keep Your Data Accurate

The accuracy of your AI models depends entirely on the quality of the data they process. This makes strong data governance an absolute must for sound decision-making.

To maintain a clear and current view of your counterparties, set up real-time data aggregation from various sources, including financial news, regulatory updates, and security bulletins. According to a Gartner survey, 45% of organizations have faced disruptions due to outdated or incomplete third-party data.

Break down data silos by standardizing data structures across platforms like GRC systems, CRMs, and ERPs. This ensures a unified, comprehensive view of your data. Additionally, validate data features carefully to avoid unintended bias. For instance, using alternative data like utility payments as "proxy variables" could skew risk assessments in unexpected ways.

Once your data is accurate and up-to-date, focus on monitoring and fine-tuning your automation to keep pace with the evolving market landscape.

Review and Adjust Your Automation

Markets evolve, and your automation must evolve with them. Regularly re-optimize your strategies - ideally every 3–6 months - using updated data to align with changing conditions. Diego Arribas Lopez captures this risk perfectly:

"Your EA risk settings from 2025 are quietly destroying your account in 2026... because the market you set them for no longer exists".

Track key metrics like win rate and profit factor over the last 50–100 trades. If your rolling Sharpe ratio falls below 50% of its backtested value, pause or re-optimize your system immediately. Keep in mind that live trading often underperforms backtests by 30–50% due to factors like slippage, spreads, and execution quality.

Implement a monthly recalibration routine that takes just 15 minutes. This should include:

- Checking your 14-period ATR against your baseline.

- Adjusting position sizes to reflect changes in volatility.

- Verifying that stop-loss distances are at least 1.5 times the average hourly range.

- Ensuring daily loss limits remain around 2–3% of account equity.

- Setting spread filters to 2x your broker’s typical active-session spread.

While automation can handle much of the heavy lifting, human oversight remains critical for high-stakes decisions. By continuously refining your system and keeping a watchful eye, you ensure your risk engine stays aligned with your business objectives.

Conclusion

Automating counterparty risk adjustments changes the way you safeguard your trading capital. Instead of depending on manual processes that can be slow and influenced by emotional decision-making, AI-driven automation creates a protective system that reacts to market changes in real time. It transforms complex market dynamics - like rising volatility, widening spreads, or vanishing liquidity - into actionable strategies that protect your account around the clock.

This approach brings clear benefits: quicker execution, removal of emotional interference, and constant monitoring - even when you’re not actively trading. With the AI trading market expected to hit $25 billion by 2026, access to tools for building such systems has never been easier. Platforms like Traidies make it simple by allowing you to describe strategies in plain language, instantly convert them into MQL5 code, and backtest using historical data - all without needing advanced programming skills.

As Trading Strategist Mauricio Vellasquez explains:

"Professional automation is not the art of taking more trades. It is the discipline of refusing the trades that should never reach the market".

An automated risk system can reject signals when the market turns unfavorable, employing safeguards like circuit breakers to pause trading if floating losses near a 5% daily drawdown limit - common for accounts funded at $100,000.

FAQs

What data do I need to automate counterparty risk?

To streamline counterparty risk management, you'll need access to data that covers creditworthiness, exposure, and transactions. Here's what that includes:

- Credit data: Information like credit ratings, scores, and other indicators of financial stability.

- Exposure data: Details on both current exposure and potential future exposure (EAD).

- Transaction details: Insights into contract types, sizes, and terms.

- Historical and market data: Data on past defaults, payment behaviors, price trends, and interest rate changes.

By analyzing these elements, you can build more accurate risk models and automate the process effectively.

How do I connect an AI model to an MQL5 trading bot safely?

To link an AI model to an MQL5 trading bot securely, start by establishing an encrypted socket connection (like SSL/TLS) to ensure data is exchanged safely. Implement authentication tokens or API keys to verify identities and restrict access strictly to necessary functions. Additionally, make sure to log all interactions for monitoring and troubleshooting purposes. Before going live, test everything in a demo environment to confirm reliability and address any potential security gaps.

How often should I retrain and re-optimize my risk settings?

It’s a good idea to regularly revisit and fine-tune your risk settings to keep up with changing market conditions. Experts recommend checking and adjusting your trading bot’s risk parameters every 3 to 6 months. This helps avoid overfitting and ensures your bot can adapt to shifts in market trends. A quarterly recalibration can be especially helpful in maintaining effective settings as volatility and market correlations evolve.