5 Ways Market Depth Impacts Trading Bots

5 Ways Market Depth Impacts Trading Bots

Market depth isn’t just a technical term - it’s a game-changer for trading bots. It shows the supply and demand at different price levels, directly influencing how bots execute trades. Ignoring it can lead to costly mistakes like slippage, execution delays, or poor strategy performance. Here’s how market depth affects bots:

- Slippage: Large orders in shallow markets can drain liquidity, forcing bots to buy or sell at worse prices.

- Execution Delays: Bots face challenges like queue positioning and flickering quotes, which slow down trades.

- Market Impact: Big trades in thin markets can move prices, increasing costs.

- Liquidity Assessment: Bots analyze depth to decide whether a trade is worth executing or not.

- High-Frequency Trading (HFT): Accurate depth data is essential for microsecond-level decisions in HFT strategies.

Each of these factors shapes how a bot performs, whether it’s minimizing costs, improving speed, or avoiding risky trades. Platforms like Traidies help traders simulate these scenarios, ensuring bots are ready for live market conditions.

5 Ways Market Depth Impacts Trading Bot Performance

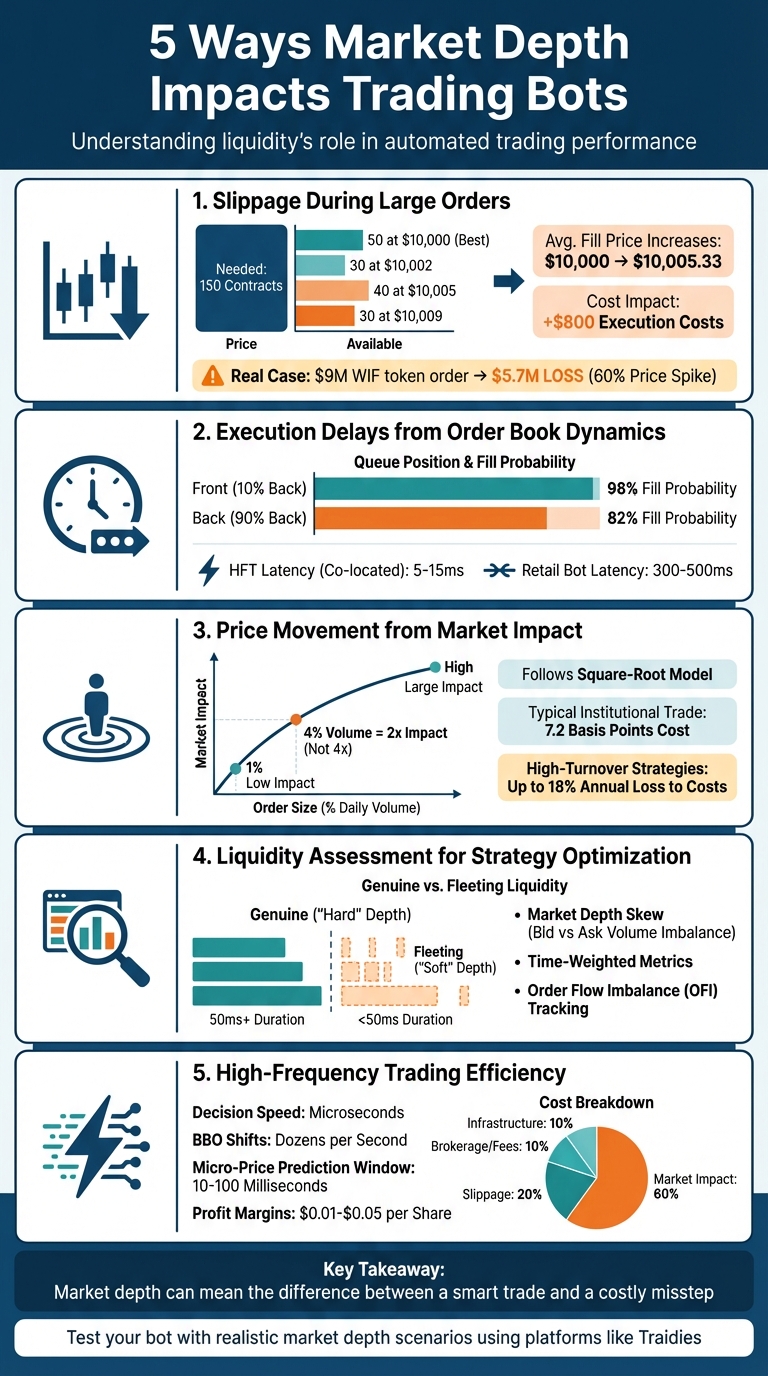

1. Slippage During Large Order Execution

Market Depth Availability

When a trading bot places a large order in a market with limited depth, it often depletes the liquidity at the best available price. For instance, if an order book lists 50 contracts at $10,000 but the bot needs to buy 150 contracts, it will have to fill the remaining orders at progressively worse prices. This could lead to an average fill price of $10,005.33, resulting in an $800 increase in execution costs. These liquidity limitations not only raise costs but also slow down execution.

"The connection between high-volume trading liquidity depth and slippage is straightforward: the deeper the liquidity, the lower the risk." - Liquidity-provider.com

Impact on Execution Speed

Market orders are designed for quick execution but often come at the expense of price control, especially in markets with shallow liquidity. Bots may choose market orders despite the higher risk of slippage or opt for limit orders, which could leave portions of the trade unfilled. To tackle this, some bots use order slicing - breaking a large order into smaller, more manageable trades - to mitigate slippage. The choice between order type and market depth plays a critical role in shaping the bot's overall strategy.

Effect on Trading Strategy Performance

Slippage can significantly impact the profitability of trading strategies. For example, in January 2024, a trader executing a $9 million market order for the dogwifhat (WIF) token suffered a $5.7 million loss due to slippage. The shallow order book caused a 60% price spike during the execution. Similarly, during the volatility of March 2020, S&P 100 stocks experienced slippage exceeding 1% on medium-sized orders as liquidity providers reduced participation.

To avoid inflated expectations, it's essential to factor realistic slippage into backtesting models. Trading bots should be configured with proper slippage tolerances and realistic execution costs. For instance, while a bot might project 15% annual returns under ideal conditions, accounting for slippage could reduce those returns by 0.5% to 3% per year. That difference could determine whether a strategy is profitable or just breaking even.

sbb-itb-3b27815

2. Execution Delays from Order Book Dynamics

Queue Position and Priority Systems

Exchanges like NYSE and NASDAQ rely on a price-time priority system, often referred to as FIFO (first-in-first-out). This means orders are executed in the order they arrive for a specific price. Even the tiniest delay - down to microseconds - can push your bot further back in the queue. For instance, in a queue of 10,000 shares, a bot positioned 10% back has a 98% chance of being filled, while one at 90% back sees its probability drop to 82%.

"Being near the front of the queue dramatically improves fill probability. This is why high-frequency traders invest heavily in latency: arriving microseconds earlier can mean the difference between the front and the back of the queue." - Michael Brenndoerfer

These timing sensitivities become even more pronounced when quotes change rapidly.

Flickering Quotes and Ghost Liquidity

High-frequency trading (HFT) often causes rapid shifts in the best bid and offer, leading to "flickering quotes" that disappear almost as quickly as they appear. Some algorithms submit and cancel orders at lightning speed, adding to the latency challenges faced by others.

HFT systems, with co-location setups, achieve latencies of 5–15ms and can complete round-trip executions in under 30ms. In contrast, retail bots using standard internet connections experience 80–100ms pings and total reaction times of 300–500ms. To avoid poor execution in thin markets, advanced bots may be programmed to skip execution entirely if market depth looks inadequate.

These rapid changes in order book data make execution more challenging, particularly when liquidity is limited.

Walking the Book in Shallow Markets

In shallow markets, placing large orders often means your bot must consume multiple price levels to find sufficient liquidity. Compounding the issue, some market manipulators use spoof orders - temporary, deceptive orders - to create the illusion of depth, leaving bots to chase liquidity that doesn't actually exist.

"The order book is not just a table of orders displayed in a terminal. It's a real-time streaming system built on state changes (event-driven), where each new order, cancellation, or execution is an event influencing other participants' behavior." - Admin, MyWinnerDays

To navigate these challenges, focus on time-weighted depth rather than relying solely on instantaneous volume. By tracking how long orders remain at specific price levels, you can separate genuine liquidity from fleeting algorithmic activity. For strategies that require a high probability of execution, consider using aggressive pricing - offering better than the current best bid or ask - to gain priority in the queue. Mastering these nuances can significantly improve your bot's performance in varying market conditions.

3. Price Movement from Market Impact

Building on the challenges of order execution, market impact plays a critical role in shaping how trading bots perform by directly affecting price movements.

Market Depth Availability

When a bot places orders that exceed the available liquidity at the best bid or ask prices, it "walks the book", consuming liquidity at progressively worse prices. For instance, in deep markets like EUR/USD, a $10 million order might have little effect on the price. However, in thinner markets such as small-cap stocks or certain corporate bonds, the same order size can trigger significant price swings.

"Shallow market depth means fewer orders at each price level. Even modest trades can move the price, leading to poor fills." – Gotrade Team

This dynamic stems from the market's depth characteristics. Interestingly, the relationship between order size and price impact isn't straightforward. Research suggests it typically follows a square-root model: trading 4% of daily volume results in about twice the impact of trading 1%, rather than four times. This highlights how market impact grows disproportionately as order sizes approach the market's typical capacity.

Impact on Execution Speed

High-frequency trading algorithms can detect large orders almost instantly, reacting by withdrawing liquidity or widening spreads - a phenomenon known as order flow toxicity. For example, a support level just a few ticks below the current price might vanish during a price probe, exposing how fleeting liquidity can be.

Orders face two types of price impacts: a temporary impact, which reflects the cost of immediate execution, and a permanent impact, where the market adjusts the price if the trade is perceived as informed. These rapid price shifts translate into real costs that can significantly influence the performance of your trading strategy.

Effect on Trading Strategy Performance

Underestimating market impact costs can turn backtested profits into losses. For example, a typical $1 million institutional equity trade incurs explicit costs of about 7.2 basis points on a round-trip. High-turnover strategies, which execute 100% of their portfolio daily, could lose up to 18% annually purely to these costs.

"A backtest is only as good as its assumptions. Transaction cost assumptions are critical and often underestimated." – Michael Brenndoerfer

To better predict short-term price movements, monitor Net Order Flow Imbalance (NOFI) - a measure of aggressive market orders versus passive limit order cancellations. Platforms like Traidies allow traders to incorporate these execution considerations during backtesting, helping ensure that bots perform more closely to expectations in live trading scenarios.

4. Liquidity Assessment for Strategy Optimization

Expanding on the relationship between market depth and slippage or execution delays, trading bots rely on liquidity assessment to fine-tune their strategies. By leveraging market depth data, these bots continuously evaluate liquidity conditions and make real-time adjustments to their execution plans.

Market Depth Availability

Bots examine the density of orders on both the bid and ask sides to assess price stability and determine whether executing a trade will significantly impact the market price. They calculate a weighted average price to ensure there’s enough liquidity to proceed with a trade. If the order book shows insufficient volume, the bot may decide not to execute the trade, thereby avoiding substantial slippage.

Advanced bots go a step further by distinguishing between "hard" depth (genuine, persistent liquidity) and "soft" depth (temporary algorithmic quotes). Using time-weighted metrics that account for order duration, they filter out misleading signals caused by spoofing - fake orders placed to manipulate liquidity perception. Additionally, bots assess market depth skew, which measures the imbalance between bid-side and ask-side volumes. For example, a heavy skew on the bid side often indicates potential upward price movement.

"Mastering order book depth is the defining factor between profitable execution and slippage losses." – QuantStrategy.io Team

By evaluating these liquidity metrics, bots can make smarter decisions about when and how to execute trades, directly influencing execution efficiency.

Impact on Execution Speed

Liquidity conditions play a major role in determining how quickly bots can execute trades. In markets with deep liquidity and a strong order book, bots can complete trades quickly with minimal market disruption. Conversely, in markets with lower liquidity, bots may face delays as they navigate limited order availability.

High-frequency trading (HFT) firms exploit tiny delays between exchanges through latency arbitrage - detecting trades on one exchange before they’re reflected on another and rapidly consuming available liquidity. To counter this, modern bots increasingly rely on time-weighted averages, focusing only on orders that remain in the book for a certain duration (e.g., 50 milliseconds). This approach helps them identify genuine structural changes and avoid reacting to fleeting, deceptive quotes.

Effect on Trading Strategy Performance

Liquidity insights significantly shape the performance of trading strategies under varying market conditions. These insights are integrated into broader bot strategies to enhance overall market outcomes. For instance, bots often use clusters of limit orders deeper in the order book as real-time support and resistance indicators, which can be more reliable than traditional price charts. By tracking the Order Flow Imbalance (OFI) - the difference between aggressive buying (market orders hitting the ask) and aggressive selling (market orders hitting the bid) - bots can anticipate short-term price changes and adjust their positions accordingly.

Sophisticated bots also spread their limit orders across a liquidity zone, improving the likelihood of favorable entry prices and successful order fills. Platforms like Traidies allow traders to incorporate these liquidity-focused strategies during backtesting, ensuring that bots perform consistently when deployed in live trading environments.

5. High-Frequency Trading Efficiency

Market depth plays a critical role in the efficiency of high-frequency trading (HFT), where decisions made in microseconds can significantly impact performance. These trading bots operate at incredible speeds - measured in milliseconds or even microseconds - making access to accurate and timely market depth data essential. By processing raw data feeds like NASDAQ ITCH or CME MDP 3.0, HFT bots create a nanosecond-accurate reconstruction of the Limit Order Book (LOB). This allows them to extract predictive signals that drive their rapid trading decisions. Unlike traditional trading, HFT operates in an environment where the best bid and offer (BBO) can shift dozens of times per second, requiring constant adaptation to these rapid changes.

Market Depth Availability

The profitability of HFT strategies hinges on the availability and depth of market data. Basic Level 1 data, which only shows the BBO, isn’t sufficient. Instead, HFT bots rely on Level 20 data (or deeper), which provides a more detailed view of the market. This allows them to assess liquidity more accurately, detect spoofing, and estimate the potential market impact before executing trades. Using this data, bots calculate a volume-weighted "Micro-Price" near the BBO to improve short-term price predictions, often within a window as tight as 10 to 100 milliseconds.

One fascinating application of this deeper data is identifying "liquidity cliffs" - price levels where available volume drops sharply. For example, in January 2026, an HFT firm analyzed a stock trading at $50.00 and spotted significant volume at $49.99 and $49.98 but only 50 shares at $49.97 before a large 10,000-share block at $49.96. The bot flagged $49.97 as a liquidity cliff, correctly predicting that a 3,000-share market sell order would bypass that level and execute at $49.96, creating notable slippage. This highlights how precision and speed in market depth analysis are indispensable for HFT.

Impact on Execution Speed

Execution speed in HFT is heavily influenced by queue position management and time priority. Bots constantly track their position in the order queue at each price level. If they fall too far back, they cancel and re-submit orders to improve their position. This requires not only fast data processing but also the ability to identify "toxic" order flow - patterns like rapid depth changes or high cancellation rates that hint at imminent market moves by informed participants.

| Cost Component | Typical Share of Institutional HFT Costs |

|---|---|

| Market Impact | 60% |

| Slippage | 20% |

| Brokerage and Fees | 10% |

| Infrastructure | 10% |

"Market impact is not just a cost - it is often the single largest hidden expense, exceeding infrastructure, exchange fees, and even adverse selection combined." – AlgoTradingDesk

During periods of high volatility, HFT bots face a unique challenge. While they often provide deep liquidity in stable markets, they’re programmed to withdraw their quotes instantly during market stress to minimize risk. This "fragile liquidity" can vanish in milliseconds, as seen during the May 2010 Flash Crash. In that event, HFT bots rapidly pulled their quotes, causing a sudden disappearance of market depth and triggering a steep, temporary market drop.

Effect on Trading Strategy Performance

HFT strategies rely on micro-level adjustments to optimize profitability, building on earlier insights into market impact and liquidity. Market depth data directly influences how these strategies perform under different conditions. For instance, in December 2025, HFT bots trading major futures contracts were observed briefly crossing quotes - where the bid equals the ask - for just milliseconds. This "zero-width spread" occurred as competing algorithms raced to capture passive flow or execute inter-market arbitrage before reverting to a standard one-tick spread. With profit margins often as slim as $0.01 to $0.05 per share in equities or $5 to $50 per lot in index futures, precision is everything.

Platforms like Traidies allow traders to integrate depth-aware execution logic during backtesting. This ensures that automated strategies account for real-world market dynamics, such as varying depth profiles, cancellation ratios, and quote velocity. By simulating these conditions, traders can refine their strategies to better handle the high-speed, competitive nature of live HFT environments.

Conclusion

Market depth plays a pivotal role in shaping trading bot performance. This article has highlighted five key ways it influences execution: slippage during large orders, delays caused by order book dynamics, price shifts due to market impact, liquidity evaluation for strategy refinement, and the efficiency of high-frequency trading. Each of these elements can determine whether your bot secures profits or suffers losses from poor execution.

Grasping order book behavior is what sets successful bots apart. As Bookmap aptly puts it, "Market depth can be the difference between a smart trade and a costly misstep". For a bot to succeed, it must interpret market depth in real time and adjust its strategy - whether that involves widening spreads in illiquid markets, identifying spoofing patterns, or pre-calculating execution prices to manage risk. This constant interaction between liquidity and execution shapes the challenges bots face in fast-moving order book environments.

The difficulty lies in the rapid pace of order book changes, which occur far more frequently than standard price ticks. A standard tick, essentially a simplified 2-level order book, often lacks detailed volume data beyond the immediate spread. Without deeper insights, bots may struggle to predict execution quality or identify liquidity cliffs, increasing the risk of slippage - issues we've already explored in discussing execution delays and market impact.

Comprehensive testing is non-negotiable. Tools like Traidies allow you to simulate market depth scenarios and test strategies under realistic conditions. These platforms let you tweak spread settings, execution modes (Aggressive, Normal, or Passive), and liquidity filters to align with the depth profile of the assets you trade. For instance, you might use a Grid -1 bps spread and Aggressive execution for highly liquid markets to reduce stalling, while opting for wider spreads and Passive fills in less liquid environments.

Before going live, ensure your bot is tested across various depth conditions to minimize slippage and execution errors. Program it to avoid trades where insufficient volume at close price levels could result in significant slippage. Rigorous testing ensures your bot can handle live market dynamics, delivering consistent performance. By mastering market depth, you’ll create bots that execute intelligently, protect capital, and adapt seamlessly to the challenges of real-world trading.

FAQs

What market depth data does my bot actually need (Level 1 vs Level 2+)?

Your trading bot needs Level 2+ market depth data to analyze order book dynamics effectively. This includes details like multiple price levels and the sizes of orders at each level. Unlike Level 1 data, which only shows the best bid and ask prices, Level 2+ data provides deeper insights into market liquidity and execution opportunities.

How can I estimate slippage and market impact before placing a large order?

To get a handle on slippage and market impact, start by diving into market depth and liquidity. The order book is your go-to tool here - it shows buy and sell orders stacked at different price points, offering clues about possible price shifts.

Next, weigh your trade size against the available liquidity. This comparison is key to understanding how your trade might affect the market. Incorporating historical or real-time data into your analysis can sharpen these estimates further. By doing so, you can tweak your order size or adjust the timing of your trades to keep slippage and market impact to a minimum.

How do bots detect spoofing or “ghost liquidity” in the order book?

Bots detect spoofing or "ghost liquidity" by examining specific patterns in trading activity. These include unbalanced order book quotes, a high number of frequent order cancellations, elevated activity levels, and repetitive cycles in market depth. Such behaviors are often red flags for manipulative strategies like layering and spoofing.