Monte Carlo Simulation for AI-Powered Trading Bots

Monte Carlo Simulation for AI-Powered Trading Bots

Monte Carlo simulation is a crucial tool for improving the performance and reliability of AI-powered trading bots. It helps traders move beyond static backtests by running thousands of randomized scenarios, providing a clearer picture of potential risks, returns, and drawdowns. This approach is particularly valuable for stress-testing trading strategies and identifying weaknesses that traditional backtesting might miss.

Key takeaways:

- Fixed Fractional Allocation (FFA): Simple to use and ensures consistent risk per trade but lacks flexibility and doesn't consider trade quality or volatility.

- Kelly Sizing: Optimizes growth by tailoring trade sizes to statistical edges but is sensitive to errors in edge estimation, potentially leading to overbetting.

- Dynamic AI-Driven Allocation: Adjusts positions in real-time based on market data, regime changes, and advanced risk metrics like VaR and CVaR, offering superior risk management but requiring complex infrastructure.

Monte Carlo simulations enhance all these methods by revealing hidden risks like sequence risk and catastrophic drawdowns. For example, if simulations show a 95% drawdown exceeding your risk tolerance, you can adjust position sizes accordingly. This ensures that your strategies are both effective and resilient in live trading environments.

Monte Carlo Simulation for Trading | Why Backtest Isn’t Enough?

sbb-itb-3b27815

1. Fixed Fractional Allocation

Fixed Fractional Allocation (FFA) is one of the simplest methods for determining how much capital to allocate per trade. With this approach, you set a fixed percentage of your total equity - usually between 1% and 2% - to risk on each trade, regardless of how strong or weak the trade signal is.

Risk Management

One of the key features of FFA is how it automatically adjusts risk as your account balance changes. For instance, if you have a $100,000 account and risk 2% per trade, a loss would cost $2,000. If your balance drops to $80,000, that same 2% risk translates to $1,600. This automatic scaling acts as a safeguard, slowing down losses during drawdowns without requiring manual adjustments.

Capital Efficiency

FFA applies a uniform treatment to all trade signals, regardless of their probability or confidence level. A trade with a 91% success prediction is allocated the same amount as one with only a 51% chance.

"A fixed fractional rule treats a 51% prediction identically to a 91% prediction, discarding the confidence information the model worked to produce." - MetaTrader 5 Machine Learning Blueprint

This "one-size-fits-all" approach has its downsides. Studies show that sticking to fixed fractional sizing instead of using more nuanced methods, like volatility-adjusted sizing, can reduce annual risk-adjusted returns by 15% to 40% and lower the Sharpe ratio by 20% to 35%.

Adaptability

FFA doesn't adapt well to changing conditions. A common workaround is discretization, where position sizes are only adjusted when changes pass a certain threshold - say, a 5% step. This can cut down on unnecessary adjustments by 60% to 80%, which in turn helps reduce transaction costs.

However, FFA has another challenge: concurrency. If a bot generates multiple overlapping signals - say, 10 trades at 10% each - the total exposure could unintentionally reach 100%, effectively leveraging the account without explicit intent.

Implementation Complexity

One of FFA's main advantages is its simplicity. By applying a fixed percentage to each trade, it requires minimal coding and is easy to implement. This makes it particularly appealing for beginners or for strategies where the trading edge hasn't been fully identified yet.

That said, FFA has its limitations. It doesn't account for variations in trade payoff structures. For instance, it treats a trade with a 3:1 reward-to-risk ratio the same as one with a 1:1 ratio, which can limit growth potential.

"Fixed fractional risks a fixed percentage of equity on every trade... Simple implementation; avoids catastrophic risk [but results in] slower growth than Kelly." - Siegfried Kamgo, Founder, FrontierWisdom

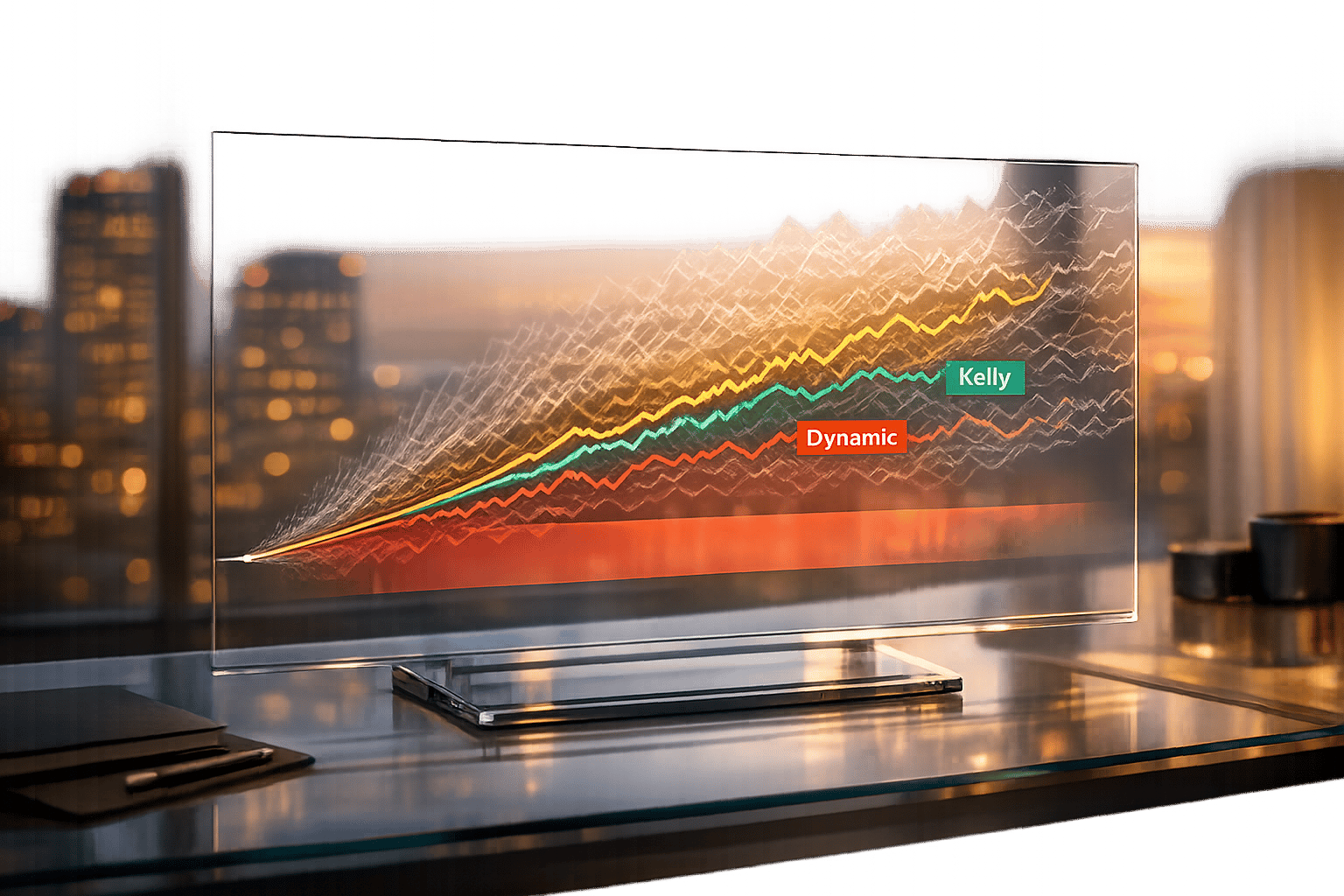

Monte Carlo simulations back this up. While FFA is effective at minimizing catastrophic losses, its static nature restricts growth. The simulations show that outcomes tend to cluster, with fewer extreme losses but also less opportunity for significant gains compared to more dynamic allocation methods. Up next, we'll see how this compares to Kelly Sizing for a more flexible approach to risk management.

2. Kelly Sizing

Kelly Sizing takes a different approach from Fixed Fractional Allocation by tailoring position sizes to the actual statistical edge of a trade. This edge is determined by combining the win probability with the payoff ratio. In simple terms, trades with higher confidence, such as those flagged by a strong AI signal, receive larger allocations, while weaker signals get smaller ones. This dynamic method naturally integrates with risk management strategies, as explained below.

Risk Management

The Kelly formula calculates the "Full Kelly" fraction, which represents the optimal bet size for maximizing long-term growth. However, using Full Kelly comes with a significant downside: a 50% drawdown is almost inevitable over time. This isn't just a rare possibility - it’s a near certainty.

To manage this risk, professionals turn to Fractional Kelly. By scaling down the Full Kelly fraction, you can still achieve strong growth with reduced volatility. For instance, Half Kelly captures about 75% of Full Kelly's growth while cutting volatility in half. Quarter Kelly, an even more cautious approach, offers 40–50% growth with much lower drawdown risk.

"Never bet more than Full Kelly, as this mathematically guarantees long-term ruin, taking you into negative expected growth territory." - Hasch74

Here’s a quick look at how different Kelly fractions balance risk and growth:

| Kelly Fraction | Aggressiveness | Growth vs. Full Kelly |

|---|---|---|

| Full Kelly | Maximum growth, maximum drawdown | 100% |

| Half Kelly | Lower variance, standard choice | ~75% |

| Quarter Kelly | Conservative for uncertain estimates | ~40–50% |

| Overbetting (>2× Kelly) | Guaranteed ruin | Negative |

Capital Efficiency

One of Kelly’s strengths lies in its ability to account for payoff asymmetry. For example, a trade with a 3:1 reward-to-risk ratio will receive a larger allocation than a 1:1 trade with the same win probability. This nuanced approach aligns well with the outputs of sophisticated AI models. Monte Carlo simulations back this up, showing how Kelly's sensitivity to payoff asymmetry boosts capital efficiency in fluctuating market conditions.

"Expected arithmetic return is not the right objective for a compounding investor; expected logarithmic growth is." - Atlas Peak Research

That said, Kelly’s precision depends entirely on accurate inputs. Overestimating your edge by just 20% can cause your growth rate to flatline, while a 30% overestimate can push it into negative territory. This makes precise probability estimation the cornerstone of any Kelly-based strategy.

Adaptability

Kelly Sizing becomes even more reliable when paired with Monte Carlo simulations. By running thousands of simulations on your trade history, you can uncover the likelihood of catastrophic drawdowns for a given Kelly fraction and identify sequence risk - something a single backtest might miss.

A practical method to enhance robustness is Bootstrap Kelly. Instead of relying on a single win-rate estimate, you resample your trade history 10,000 times and use the 5th percentile of the resulting Kelly distribution as your operating fraction. This approach builds in a natural safety margin, protecting against overfitted AI models.

"The distance between 'I have edge' and 'I don't' is smaller than your confidence interval. A fixed fraction ignores this entirely." - Python Quant

These adaptability techniques help address real-world challenges and make Kelly Sizing more practical for live trading environments.

Implementation Complexity

Applying Kelly Sizing in live AI systems introduces unique challenges. For instance, when multiple overlapping signals are generated, independently applying Kelly to each can result in excessive portfolio exposure. The solution is to average allocations across active signals and apply correlation adjustments when signals are strongly related (e.g., correlation coefficients above 0.7).

Another issue is overtrading. Since position sizes shift every time an AI model updates its probability estimates, frequent adjustments can lead to high transaction costs. To counter this, adjustments should only be made when changes exceed a 5% threshold. Additionally, setting a hard cap - such as limiting any single trade to 5% of total capital - can safeguard against major losses caused by an overly confident AI error.

3. Dynamic AI-Driven Allocation

Dynamic AI-Driven Allocation offers a step forward from the static methods of Fixed Fractional Allocation (FFA) and Kelly Sizing. Instead of relying on fixed percentages or formulaic approaches, this system adjusts position sizes continuously, leveraging live market data, regime detection, and Monte Carlo simulations.

Risk Management

This method builds on the foundations of FFA and Kelly Sizing by incorporating real-time risk metrics. A key component is the use of Value at Risk (VaR) and Conditional Value at Risk (CVaR). These metrics are calculated using Monte Carlo simulations and serve as strict thresholds. For instance:

- Trades are blocked if 95% VaR exceeds 2% of total equity.

- Similarly, trades are halted if CVaR - the average loss in the worst 5% of scenarios - exceeds 3% of equity.

The system also integrates regime detection, categorizing markets into BULL, BEAR, or VOLATILE conditions. This allows for automatic adjustments between aggressive and defensive strategies. As Strategy Arena explains:

"The leader in a bull market is often a laggard in a bear market. Smart Portfolio aims for consistent performance across regime changes."

By accounting for market regimes, this approach reduces the risk of unexpected drawdowns and smooths the portfolio's performance over time in ways that FFA or Kelly Sizing alone cannot achieve.

Capital Efficiency

Dynamic systems aim to maximize long-term growth by calculating the optimal "Kelly Edge" in real time. They also monitor correlations between active strategies. If two strategies are closely correlated, the system reduces the allocation to the weaker performer, prioritizing the one better suited to the current market regime.

For example, a portfolio of 5–7 AI strategies, when properly allocated, tends to experience smaller maximum drawdowns compared to any individual strategy within it.

Adaptability

A standout feature of this approach is its adaptive Monte Carlo engine, which adjusts historical trade data to reflect current market volatility. This is crucial because basic Monte Carlo simulations often underestimate drawdowns by as much as 40% when they fail to account for volatility clustering.

To address this, advanced systems use block bootstrap methods, sampling sequences of trades rather than individual ones. This preserves the natural streaks of wins and losses seen in real markets. A 2026 study by Soroush Shahsafi and Farnoosh Naderkhani at Concordia University highlighted that separating asset selection from capital allocation produced the most consistent risk-adjusted returns.

Implementation Complexity

Dynamic AI-Driven Allocation is technically demanding. Reinforcement learning (RL) models that attempt to assign exact portfolio weights often face challenges with computation and convergence, especially as the number of assets increases. A practical workaround is a two-step process:

- Use a discrete AI agent to generate buy/sell signals for asset selection.

- Apply a classical optimizer (e.g., Sharpe Ratio Maximization or Risk Parity) to calculate precise allocation weights.

As Shahsafi and Naderkhani observed:

"RL agents often struggle with multi-asset allocation, generating noisy portfolios, while classical optimization techniques provide precision... but do not provide dynamic selection."

System reliability is another critical factor. AI-driven bots can lose track of key risk states - such as daily loss limits or high-water marks - if not properly configured. To counter this, deterministic fallbacks are often implemented, ensuring the system reverts to a baseline strategy if its risk-adjusted performance turns negative. Reliable tail-risk metrics, such as the probability of ruin, require at least 10,000 simulations for accuracy, though 1,000 is often used as a practical minimum.

| Metric | Purpose | Pass Threshold |

|---|---|---|

| VaR 95% | Worst expected loss at 95% confidence | < 2% of equity |

| CVaR (ES) | Average loss in the worst 5% of paths | < 3% of equity |

| Probability of Ruin | Chance of losing > 50% of capital | < 1% |

| Kelly Edge | Optimal size for long-term growth | > 0.10 |

| Fragility Score | Sensitivity to market regime changes | < 60% |

This dynamic framework enables robust monitoring and adaptability in live trading environments. Platforms like Traidies are already utilizing such systems, allowing traders to automate and fine-tune strategies while maintaining strong, real-time risk management capabilities.

Pros and Cons of Each Technique

Fixed Fractional vs Kelly Sizing vs Dynamic AI-Driven Allocation

Here’s a breakdown of the strengths and drawbacks of each allocation method, building on the earlier analysis.

Fixed Fractional Allocation (FFA) is straightforward and ensures consistent risk per trade. Its simplicity makes worst-case losses predictable, which is a major plus for risk-averse traders. However, it doesn’t account for differences in signal quality, asset volatility, or correlations between assets. By treating all signals the same, it limits the potential for long-term growth.

Kelly Sizing focuses on maximizing growth by tailoring allocations to a trade’s statistical edge. While this can be highly effective, even small errors in estimating your edge can lead to overbetting and significant losses. Many experts recommend using Full Kelly as a ceiling for aggressiveness rather than a standard approach:

"The Kelly Criterion should usually be read as an upper bound on aggressiveness, not as a default deployment weight." - ML4T, 3rd Edition

For a more balanced approach, Half-Kelly is often preferred. It captures about 75% of the potential growth while reducing portfolio volatility significantly.

Dynamic AI-Driven Allocation stands out by adapting to live data, model confidence, and shifting market conditions. This method addresses the shortcomings of the others, optimizing both risk management and capital use. However, it requires a complex system to function effectively. Studies have shown that dynamic frameworks can outperform simple equal-weight strategies by 15–40% in annual risk-adjusted returns.

Here’s a quick comparison of the three methods:

| Feature | Fixed Fractional | Kelly Sizing | Dynamic AI-Driven |

|---|---|---|---|

| Risk Management | Predictable risk per trade but overlooks asset-specific factors | Growth-focused but sensitive to edge miscalculations | Adaptive and aware of market conditions |

| Capital Efficiency | Limited upside | Theoretically ideal for growth | High - adjusts with model confidence |

| Adaptability | Rigid, rule-based | Moderately flexible with reliable stats | Highly responsive to market shifts |

| Implementation Complexity | Minimal | Moderate - requires statistical inputs | High - needs an ML pipeline and fine-tuning |

The best method depends on where you are in your trading journey. For beginners or those with unproven strategies, Fixed Fractional Allocation is a reliable starting point. As your confidence and statistical data improve, Fractional Kelly offers a more growth-oriented option. For those with robust datasets and advanced tools, Dynamic AI-Driven Allocation delivers superior results. However, it demands a strong infrastructure, including a simulation engine and at least 1,000 Monte Carlo iterations to ensure reliable outcomes. These findings emphasize the need to align your approach with solid risk management practices, particularly in AI-driven trading.

Conclusion

When it comes to capital allocation, the best strategy evolves as your trading skills and data reliability improve. For beginners or those using untested bots, Fixed Fractional Allocation is a great place to start. By limiting risk to 1–2% per trade, you can focus on gathering real performance data without exposing yourself to significant losses. Once you've established a solid edge, Fractional Kelly (usually between 0.25x and 0.5x) becomes a more effective way to grow your capital while avoiding the high drawdown risk associated with Full Kelly. For advanced traders managing multi-asset AI bots with reliable confidence signals, Dynamic AI-Driven Allocation offers a way to achieve better risk-adjusted returns - provided you have the right infrastructure in place.

One constant across all methods is the importance of Monte Carlo simulation. This tool is crucial for testing and validating position sizing. Instead of relying on a single backtest, Monte Carlo simulation generates thousands of scenarios to reveal realistic drawdown risks. It's wise to base your position sizing on the P95 drawdown rather than the average results. For instance, if your tolerance is a 25% loss but simulations show a P95 drawdown of 42%, you should reduce your position size to about 60% of your original plan. Additionally, aim to keep your ruin probability below 1%. If more than 1% of simulations result in catastrophic losses, your sizing is too aggressive, no matter the method. Always run enough simulation iterations to account for tail risks effectively.

Platforms like Traidies simplify this process by integrating AI-powered strategy building, MQL5 code generation, and automated backtesting. These tools provide the data foundation you need to perform meaningful Monte Carlo analysis before going live with your strategy.

FAQs

How many Monte Carlo runs do I need to trust the drawdown results?

To get dependable drawdown results, it's best to run at least 1,000 Monte Carlo simulations. However, using 5,000 to 10,000 simulations can deliver more consistent and precise estimates of tail risks. Running a higher number of simulations boosts confidence in the outcomes when evaluating trading strategies.

When should I use fixed fractional vs fractional Kelly sizing?

Fixed fractional sizing involves risking a consistent percentage of your capital on each trade, typically around 1-2%. This approach provides a stable framework and helps keep drawdowns predictable. It’s particularly useful for strategies that are either untested or where the potential edge is uncertain.

On the other hand, fractional Kelly sizing adjusts position sizes according to the estimated edge and confidence level. This method aims to maximize growth while still keeping drawdowns under control. It’s best suited for systematic strategies where the edge has been statistically validated, allowing for dynamic and efficient capital allocation.

How can I handle overlapping AI signals without overexposure?

To handle overlapping AI signals and prevent overexposure, it's crucial to analyze how signals interact and ensure genuine diversification across assets, timeframes, and strategies. Tools like correlation matrices and portfolio scoring can help pinpoint areas where overlaps might occur. Additionally, running Monte Carlo simulations allows you to test how your portfolio performs under different conditions, revealing potential weaknesses.

Regularly monitoring and adjusting strategies is essential. By addressing gaps and lowering correlation, you can maintain a well-balanced approach to capital allocation.