MQL5 Parameter Tuning: Best Practices

MQL5 Parameter Tuning: Best Practices

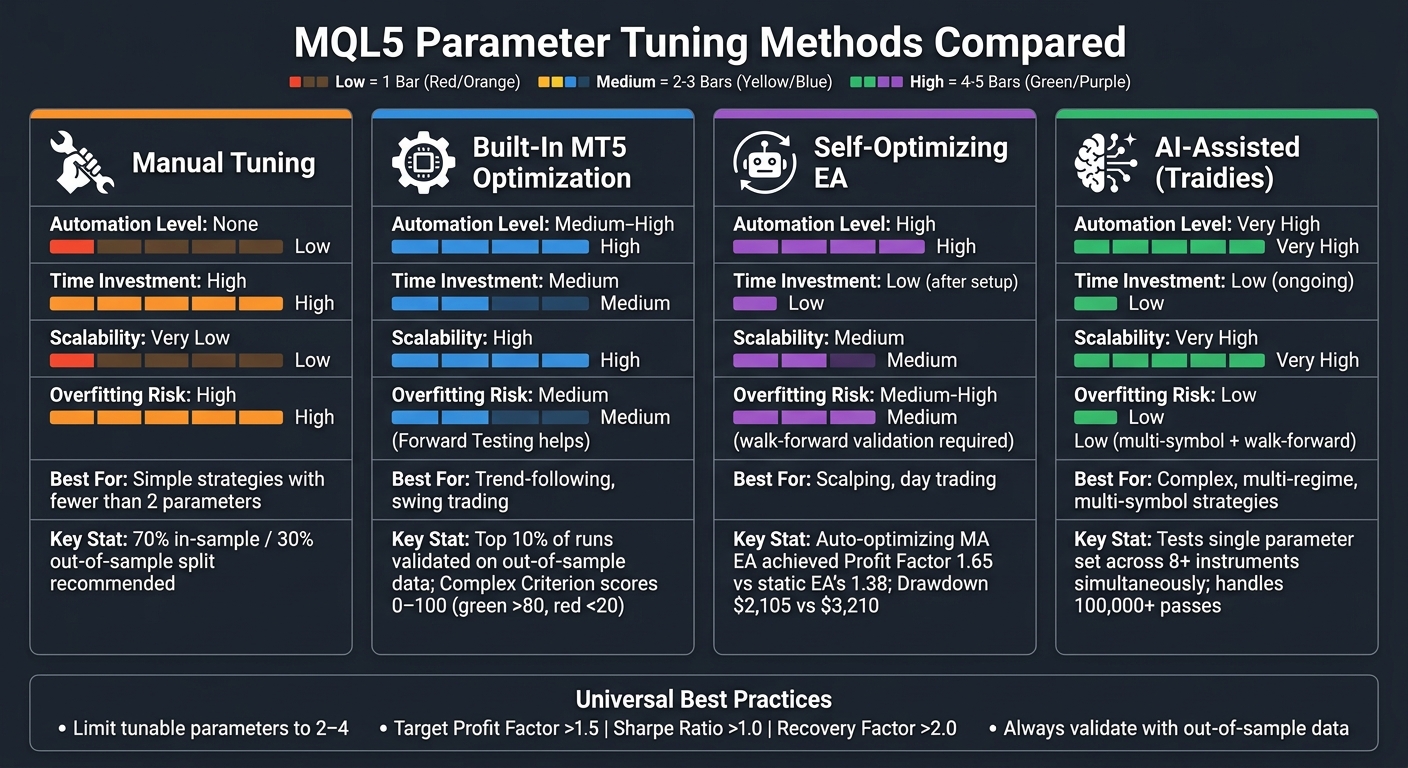

If your trading strategy performs well in backtesting but struggles when live, the problem might lie in how you configure its parameters. Tuning inputs like moving averages, RSI thresholds, and stop-loss levels is critical to achieving consistent results. This guide explains four methods for optimizing parameters in MQL5:

- Manual Tuning: Full control but time-intensive and prone to overfitting.

- MT5 Built-In Optimization: Automates testing with tools like genetic algorithms and forward testing to reduce overfitting risks.

- Self-Optimizing EAs: Automatically adjust parameters during live trading but require careful setup to avoid overfitting.

- AI-Assisted Tools (e.g., Traidies): Use AI for fast, multi-symbol optimization with minimal manual effort.

Each method has its strengths and limitations. The right choice depends on your strategy's complexity and your time investment. For U.S. traders, adapting these methods to comply with FIFO rules and accounting for slippage or spread widening is essential. Always validate results with out-of-sample testing and aim for stable parameter ranges.

Optimized RSI Trading Strategy: A Comprehensive Backtesting Guide in MQL5 using optimizer

sbb-itb-3b27815

1. Manual Parameter Tuning in MQL5

Manual parameter tuning in MQL5 involves using the MT5 Strategy Tester to fine-tune your Expert Advisor (EA). The process includes selecting the EA, setting a date range for testing, and manually defining the start, step, and stop values for each input. After running the backtest, you review the results and adjust parameters until you find what seems like the best configuration. While this method gives you full control, it has clear limitations, including scalability issues and the risk of overfitting.

Automation Level

This approach is entirely manual, requiring you to define all parameter ranges in the "Inputs" tab. Since no algorithms are involved, every input must be adjusted and interpreted by hand. While this level of control can be helpful for simple setups, it can also be a bottleneck when dealing with more complex configurations.

Scalability

Manual tuning works well when you're dealing with just one or two parameters. However, as you add more variables, the number of possible combinations grows exponentially, making it nearly impossible to test all options effectively.

"Running backtests multiple times for every possible combination and permutation of input parameters can be time-consuming and inefficient, often leading to overfitting or suboptimal strategies." - Prashanth Noble Bose

This exponential growth in complexity makes manual tuning impractical for strategies with many parameters.

Risk of Overfitting

Overfitting becomes a major concern with manual tuning. By focusing on parameter values that perform well in historical backtests, you might inadvertently tailor the strategy to market noise rather than genuine patterns. The more parameters you adjust, the easier it is to create a strategy that fits past data perfectly but fails in real-world conditions.

One way to spot potential overfitting is by checking parameter stability. For example, if a moving average period of 20 performs well, but 19 and 21 do not, that’s a warning sign. A robust strategy should show consistent performance across a range of parameter values, not just a single point.

Robustness of Results

The ultimate test of any strategy is its performance on unseen data. To evaluate robustness, split your historical data into two parts: 70% for optimization (in-sample) and 30% for validation (out-of-sample). If the strategy’s performance on out-of-sample data drops significantly - say, below 80% of its in-sample performance - it’s likely overfitted.

Key metrics to aim for after tuning include:

- Profit Factor: Above 1.5

- Sharpe Ratio: Above 1.0

- Recovery Factor: Above 2.0

Testing the strategy across different market conditions is another way to ensure robustness. For instance, compare its performance in the volatile markets of 2022 with the trending conditions of 2020. This helps confirm that the parameters work across various scenarios and aren’t just tailored to specific historical periods.

Understanding these limitations and challenges is crucial before diving into automated methods. Manual tuning, while straightforward, comes with trade-offs that make it less suitable for complex strategies or larger parameter sets.

2. Built-In MT5 Optimization Methods

MT5's Strategy Tester takes the hassle out of manual testing by automating the parameter search process. Instead of tweaking values one at a time, it runs through thousands of parameter combinations automatically, presenting the top-performing results for you to analyze.

Automation Level

All you need to do is define the input ranges, and the tester handles the iterations. For more advanced setups, you can fine-tune the search space programmatically using functions like ParameterSetRange and ParameterGetRange within the OnTesterInit handler. If the default optimization metrics don’t align with your strategy, you can use the OnTester() function to create a custom metric tailored to your specific needs.

MT5 provides three optimization modes to suit different scenarios:

- Slow Complete Algorithm: Offers precise results but can be time-consuming for complex strategies.

- Fast Genetic Algorithm: Leverages evolutionary techniques to identify strong parameter sets much faster, ideal for large search spaces.

- Math Calculations: Skips price history entirely, focusing on mathematical models or custom functions instead.

This automation not only simplifies testing but also allows you to tackle even the most intricate strategies efficiently.

Scalability

The Strategy Tester’s multi-threaded design ensures scalability by running multiple passes in parallel across all available CPU cores. If your local hardware isn’t sufficient, you can connect remote agents or utilize the MQL5 Cloud Network, which gives you access to thousands of agents worldwide for massive parallel processing. Each agent operates independently, ensuring no interference between concurrent runs.

For most traders, the Fast Genetic Algorithm strikes the perfect balance between speed and accuracy. What might take years with a full search can often be completed in just hours, delivering results that are nearly as reliable.

Risk of Overfitting

Overfitting is a common pitfall in optimization, but MT5 addresses this with Forward Testing. This feature splits your historical data into two segments: the first is used for optimization, while the second validates the top results. Typically, the top 10% of runs from a full search or the top 25% from a genetic algorithm are tested on the out-of-sample data. This approach ensures that the optimized results are better suited for live trading.

"Overfitting is a major risk in any optimization process. An overfitted EA may perform exceptionally well on historical data but fail when faced with new market conditions." - Javier Santiago Gaston de Iriarte Cabrera

To further reduce the risk of overfitting, limit the number of parameters you optimize at once. Focusing on two or three critical inputs - such as an indicator period or a key logic threshold - can help you avoid accidentally overfitting to historical data.

Robustness of Results

MT5 allows you to optimize for metrics that emphasize stability over raw profit. The Complex Criterion is especially useful, as it combines factors like the number of trades, drawdown, recovery factor, expected payoff, and Sharpe ratio into a single score ranging from 0 to 100. Scores above 80 are highlighted in dark green, indicating strong combinations, while scores below 20 are marked in red. These integrated metrics help ensure that your optimization results are robust enough for live trading.

| Optimization Criterion | What It Measures |

|---|---|

| Balance max | Highest final account balance |

| Profit Factor max | Ratio of total profit to total loss |

| Drawdown min | Lowest relative drawdown percentage |

| Sharpe Ratio max | Risk-adjusted return |

| Complex Criterion max | Combined score across trades, drawdown, recovery, payoff, and Sharpe ratio |

| Custom max | Value returned by OnTester() in your EA code |

One practical feature of MT5 is its ability to save all optimization results in .opt cache files. This means you can pause a long optimization run and resume it later without having to start over, making it much easier to handle large parameter spaces without losing progress.

3. Self-Optimizing EAs in MQL5

Self-optimizing Expert Advisors (EAs) bring a new level of adaptability to trading by automatically adjusting their parameters during live trading. Unlike manual or built-in optimizers, these EAs operate as independent systems, tweaking their strategies in real-time based on market conditions. This can happen at set intervals, such as daily, hourly, or after completing a specific number of trades.

"Self-optimization in an EA is a process involving the EA adapting its trading strategy parameters to achieve better performance based on historical data and current market conditions." - MQL5 Article

Automation Level

The framework of a self-optimizing EA includes several key components: a manager to oversee operations, an optimization algorithm (like Gradient Descent or Nelder-Mead), and a virtual EA to simulate trades. The process is controlled using the OnTimer() handler, which schedules re-optimization. Functions like ParameterGetRange and ParameterSetRange allow the EA to define and adjust its input parameters.

To handle indicators, calculations must be embedded directly into the EA’s code. Standard indicator handles aren't suitable here because they can't be deleted within the Strategy Tester. Running thousands of internal iterations without this adjustment could quickly overwhelm system resources like RAM.

Scalability

The simplest method for optimization is using internal brute-force loops, but this approach is limited by the processing power of a single CPU core. A more efficient solution involves external execution. In this setup, a primary MT5 instance triggers a secondary Tester instance, which utilizes the full Strategy Tester engine with multi-threaded agents.

For example, the BuddyIlan EA, trading EURGBP on the M15 timeframe, used this method. Every Saturday at 6:00 AM, it optimized four parameters - Stop Loss (SL), Take Profit (TP), STOFilter, and STOTimeFrameFilter. This process resulted in a profit of $2,343.52 with a drawdown of 15.03%. To maintain the EA's responsiveness, heavy optimization tasks should be scheduled during off-market hours. However, while scalability improves performance, it also raises the risk of overfitting.

Risk of Overfitting

Frequent re-optimization can lead to overfitting, where the EA becomes too tailored to past data and struggles in live markets. To reduce this risk, it's best to limit the number of adjustable parameters to 2–4 and restrict the range of adjustments in each cycle. Walk-forward validation is a reliable method for mitigating overfitting. This involves optimizing on one segment of data and testing on the next to ensure the strategy performs well on unseen data.

"An EA whose performance changes sharply after a small parameter change may be over-optimized." - trgy.co.jp

Robustness of Results

A long-term backtest on EURUSD H1 demonstrated the advantages of self-optimizing EAs. The auto-optimizing Moving Average EA achieved a profit factor of 1.65 with a maximum drawdown of $2,105, outperforming its static counterpart, which had a profit factor of 1.38 and a drawdown of $3,210. Testing across multiple symbols can further validate an EA’s robustness, as it needs to handle varying market conditions effectively.

While self-optimizing EAs offer the benefit of continuous adaptation, they come with challenges like overfitting. By balancing dynamic adjustments with careful parameter management and validation, traders can harness their potential while minimizing risks. This approach complements other optimization methods, providing a unique blend of adaptability and performance in live trading scenarios.

4. AI-Assisted Parameter Tuning with Traidies

Traidies offers a fresh approach to parameter tuning by blending AI-driven code generation with optimized workflows. With Traidies, you can describe your trading strategy in plain language, and it will automatically generate MQL5 code while optimizing parameters. It combines the precision of manual tuning, the speed of built-in optimization tools, and the flexibility of self-optimizing EAs into one powerful, AI-driven platform.

Automation Level

Traidies simplifies the tuning process with auto-optimizing algorithms that adjust parameters based on live market conditions after trades are executed. This minimizes the need for constant manual oversight. The platform’s AI Strategy Parser takes natural language descriptions of strategies and converts them directly into MQL5 code, including parameter ranges and input definitions - eliminating the need for hand-coding.

Scalability

Thanks to cloud-based processing via WebRequest and support for multi-symbol optimization, Traidies can handle even the most complex parameter spaces efficiently. It validates performance across multiple instruments, ensuring robust results. For parameter spaces with over 100,000 passes, Traidies tests a single parameter set across eight or more instruments simultaneously, reducing the risk of results being skewed by a single currency pair’s anomalies.

Risk of Overfitting

To avoid overfitting, Traidies recommends limiting tunable parameters to two to four. It employs walk-forward optimization to validate strategies. This involves dividing historical data into segments and testing on unseen data after each optimization pass. Additionally, strategies are validated across three distinct phases: Development, Confirmation, and Unknown (Out-of-Sample) periods.

Robustness of Results

The platform focuses on selecting stable parameter ranges where performance remains consistently reliable. This approach ensures that the chosen parameters aren’t just optimized for historical data but can withstand slight variations in market conditions.

"Backtesting in MT5 allows you to rigorously test strategies on historical data, revealing their true edge before risking real capital." - Saeid Soleimani

Pros and Cons of Each Approach

MQL5 Parameter Tuning Methods Compared: Manual vs MT5 vs Self-Optimizing vs AI

When it comes to optimizing MQL5 Expert Advisors, each parameter tuning method has its own set of strengths and weaknesses. The choice of method depends on factors like the complexity of your strategy, the time you can dedicate, and how volatile the market is.

Here’s a quick breakdown of how the approaches compare:

| Approach | Automation Level | Time Investment | Scalability | Best Fit For |

|---|---|---|---|---|

| Manual Tuning | None | High | Very Low | Simple strategies with fewer than 2 parameters |

| Built-in MT5 (Genetic) | Medium–High | Medium | High | Trend-following, swing trading |

| Self-Optimizing EA | High | Low (after setup) | Medium | Scalping, day trading |

| AI-Assisted (Traidies) | Very High | Low (ongoing) | Very High | Complex, multi-regime, multi-symbol strategies |

Each method balances control, speed, and complexity differently, so let’s dive into the details.

Manual tuning offers complete control, but it’s incredibly time-consuming. Its limited scalability makes it suitable only for very simple strategies. If your strategy has fewer than two parameters, manual tuning can help verify the basic logic before you move on to more advanced optimization.

Built-in MT5 optimization is a middle ground for many traders. The platform’s genetic algorithm is particularly useful when you’re dealing with extensive parameter combinations - think over 100,000 passes. This approach works well for trend-following and swing trading strategies, which don’t require constant updates.

Self-optimizing EAs shine in fast-moving markets. As Javier Santiago Gaston de Iriarte Cabrera explains, "The EA auto-adapts to the current market environment, reducing always on manual supervision and parameter change." However, the tradeoff is added code complexity, which can strain system resources if not managed carefully.

AI-assisted tuning tackles the challenges of large datasets and multi-symbol strategies with ease. It excels in adapting to regime changes and validating strategies across multiple symbols - all with minimal manual effort. The downside? You need to trust the AI’s logic. This makes transparency and proper validation methods, like walk-forward testing, absolutely critical.

Conclusion

Every method outlined in this article caters to specific market scenarios, and combining them thoughtfully can deliver the most effective results. The strategies discussed blend AI-assisted tools with more traditional optimization techniques, offering a well-rounded approach to trading.

For U.S. traders, adapting these strategies to the local regulatory and market environment is essential. Start by leveraging AI-powered platforms like Traidies to quickly prototype strategies in natural language and convert them into MQL5 code. Once you have an EA ready, use MT5's genetic optimizer with a 70/30 in-sample/out-of-sample split. This step ensures your strategy isn't just overfitting historical data but has robust parameter ranges, as detailed in the MT5 optimization section. Finally, deploy a self-optimizing EA that can adjust dynamically in real time, eliminating the need for constant manual tweaks - an approach highlighted in the self-optimizing EA section.

It's also crucial for U.S. traders to ensure their EAs comply with netting account requirements under FIFO rules and include safeguards against spread widening during major economic events like Non-Farm Payrolls or Federal Reserve announcements.

"Optimization is not merely about finding parameters that show the highest profit on historical data; that path often leads to curve-fitting." - Trading Strategies Academy

Keep your parameters simple - limit them to 2–4 - and aim for consistent performance across a range of conditions rather than chasing isolated peaks. Always validate your results with out-of-sample data. The ultimate goal isn't a flawless backtest; it's creating a strategy that can endure when the market behaves unpredictably.

FAQs

How do I pick the right parameter ranges to optimize?

To select parameter ranges in MQL5, prioritize stable and realistic values rather than aiming solely for maximum profits. Start by defining initial ranges that align with your strategy's logic. Then, refine these ranges using tools like ParameterGetRange() during the OnTesterInit() phase. To avoid overfitting, keep the number of parameters to a minimum, divide test periods, and check for consistent performance across similar values. This method enhances reliability and helps steer clear of over-optimization pitfalls.

What’s the fastest way to tell if my EA is overfitted?

The fastest way to spot overfitting in your EA is by conducting out-of-sample testing. Here's how it works: take the optimized parameters and apply them to a completely different data period. If you notice a significant drop in performance, it's a strong sign of overfitting. This method helps confirm that your EA isn't overly customized to past data and can handle new, unseen scenarios.

When should I use a self-optimizing EA instead of MT5 optimization?

When you're looking for a trading algorithm that can adjust dynamically to market changes during live trading, a self-optimizing EA is the way to go. It fine-tunes its parameters in real-time, often relying on recent data, which significantly reduces the need for manual adjustments.

In contrast, MT5 optimization happens offline, before trading begins. It uses historical data to determine the best parameters for your strategy. While MT5 optimization is ideal for setting up your strategy initially, self-optimization shines when ongoing adjustments are needed to keep up with market fluctuations. Each approach has its place, depending on your trading needs.